SRS Account Hack: Why You Should Top Up $1 to Your Supplementary Retirement Scheme Account

You’ve probably read or heard this advice many times in Seedly or even among your savvier circle of friends.

Top up $1 to your Supplementary Retirement Scheme (SRS) account to lock in your retirement age!

Wondering why you should do that?

Hint: It’s to do with retirement planning and massive tax savings if you play your cards right

To help you, I’ll even show you a step-by-step guide on how to open an SRS account.

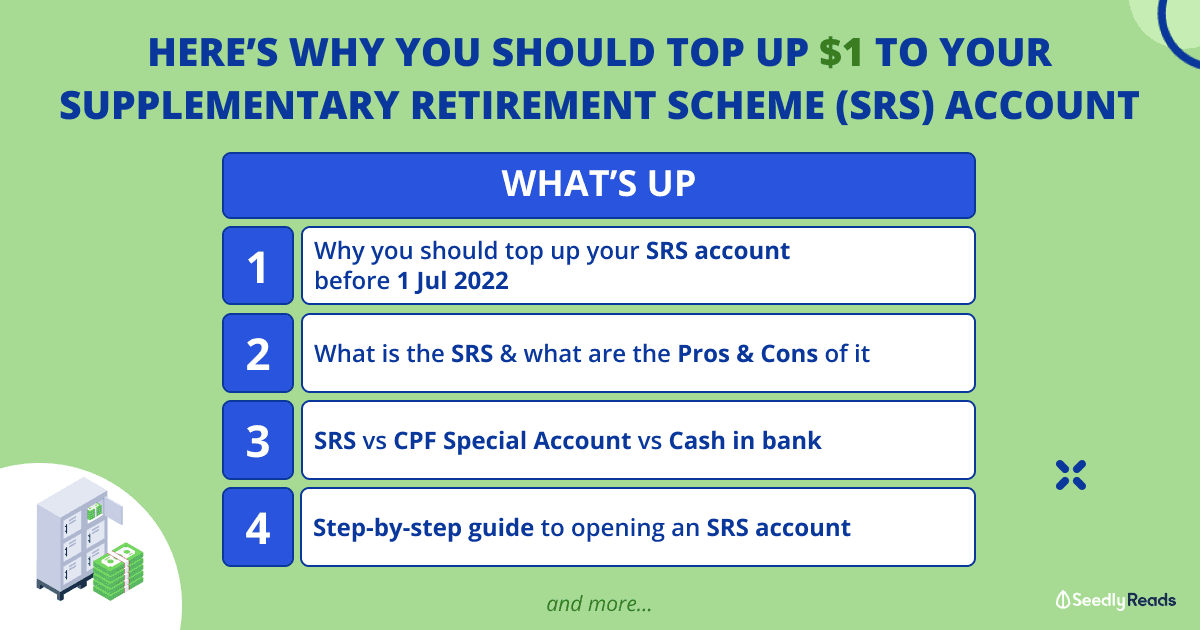

TL;DR: SRS Account Hack — Here’s Why You Should Start Your Supplementary Retirement Scheme Account With $1 Now

With an SRS account, you can:

- Reduce your taxable income by up to $15,300 every year for Singaporeans and $35,700 a year for foreigners

- note that the annual personal income tax relief cap of $80,000 applies

- Invest your SRS monies and enjoy tax-free returns

- Currently, you will only need to pay personal income taxes if you earn more than $20,000 per year. When you retire and do not have any personal taxable income, you can withdraw up to $40,000 per year from your SRS account tax-free on or after reaching the statutory retirement age (63 years old in 2022). That’s $400,000 over 10 years tax-free.

You can open it anytime.

So why do it now?

Well… it’s all thanks to this particular paragraph that I found in a 29-page PDF put up by the Ministry of Finance:

Government policies are updated often, so we never know when they might raise the current statutory retirement age from 62 to something higher.

.

.

.

Oh, wait… they ALREADY did.

Retirement Age Singapore (2022) and Link to the SRS Scheme

Yep, the statutory retirement age will be raised from 62 to 63 from 1 July 2022 and further increased to 65 by 2030.

So if you want to be able to withdraw your SRS monies at 62, you should make your first contribution to your SRS account before 1 July 2022.

IF you’re on the fence about this, your first contribution could be as little as $1.

Just don’t put more than that if you haven’t figured out how your SRS account can help you in retirement planning yet.

Interested?

Here’s what you need to know!

SRS Singapore Explained: What is an SRS Account?

The Supplementary Retirement Scheme was started in 2001 and is part of the Singapore government’s multi-pronged strategy to address the financial needs of a greying population.

It’s basically a way to help Singaporeans save more for their old age.

Of course, they are over and on top of their Central Provident Fund (CPF) monies.

Think of the SRS as an extra savings and investment account for retirement planning.

It is a purely voluntary scheme, unlike our CPF, where you can contribute any amount subject to a cap of $15,300 yearly.

You can choose to open your SRS account with any of the following banks in the private sector: DBS, OCBC, or UOB.

You’ll only earn the standard 0.05% p.a. return as you would with a regular bank savings account.

But if you want to, you can also use your SRS monies to invest in various financial instruments and products to increase your returns.

What Is the Difference Between Topping Up SRS Account vs CPF Special Account vs Holding Onto Cash?

When it comes to retirement planning and tax savings, many people are confused between topping up their SRS Account vs their CPF SA.

I’ve created this comparison table to give you a better overview of the difference and the potential returns you can get:

FYI: I’ve also included holding onto cash in your bank savings account as a point of reference.

| SRS vs. CPF vs. Cash | Supplementary Retirement Scheme (SRS) | CPF Special Account (CPF SA) | Cash (Savings Account) |

|---|---|---|---|

| Interest Rate | 0.05% p.a. Note: returns can be higher depending on what you choose to invest in | 4% p.a. | 0.05 to 1+% p.a. (realistic) |

| Yearly Contribution Cap For Tax Relief | $15,300 (Personal) | $16,000 ($8,000 Personal + $8,000 Family) | No |

| Tax Deductible? | Yes | Yes | No |

| Withdrawal Conditions | At 62 years old (retirement age) Note: if withdraw before, subject to 5% penalty | At 65 years old (default) At 55 years old ($5,000 if you have not met Full Retirement Sum FRS or Basic Reitrement Sum BRS with pledging of property. If you have met either one you can withdraw any amount above the sums) | Anytime |

| How To Start | Open with DBS, OCBC, or UOB | Automatically enrolled for Citizens or PR | Open with any bank |

Regardless of what you do, don’t just leave your money in your regular bank savings account, which only gives you a paltry 0.05% p.a.

At least put it into a high-interest savings account while you figure out if you want to do an SRS or CPF SA top-up.

Now that you have an overview, here’s a more in-depth look at the three options I’ve presented to you.

1) Supplementary Retirement Scheme (SRS) Investment, Tax Relief, Max SRS Contribution and More

What is the Benefit of SRS Account:

- You can lock in your retirement age at 62 years old if you make a $1 top-up before 1 July 2022

- You can save more on tax every year with a higher contribution amount compared to topping up your CPF SA, i.e. reduce your taxable income by up to $15,300 every year for Singaporeans and $35,700 a year for foreigners

- You can withdraw your money before the age of 62 years old if you need the money urgently. But, you will need to pay a 5% penalty fee, and you will be taxed 100% on these withdrawals

- Currently, you will only need to pay personal income taxes if you earn more than $20,000 per year. This means that when you retire and do not have any other taxable income and relief, you can withdraw up to $40,000 per year from your SRS account tax-free on or after reaching the statutory retirement age (63 years old from 1 July 2022). That’s $400,000 over 10 years tax-free!

Cons of Putting Money Into SRS Account & How to Invest in SRS:

- You get 0.05% p.a. like a regular bank savings account

- You can choose to invest your monies, but the investment returns are non-guaranteed because they depend on your investment decisions.

SRS Funds Withdrawal Rules

Also, here are the SRS withdrawal rules you need to take note of:

| Type of Withdrawal | Amount Subject to Tax | 5% Penalty Imposed? |

|---|---|---|

| Withdrawal on or after the prescribed retirement age (withdrawal can be spread over 10 years from the date of first penalty-free withdrawal) | 50% of the withdrawal sum (capped at $400,000 over 10 years) | No |

| Withdrawal on medical ground (physical or mental incapacity; partial withdrawal on the grounds of terminal illness) | 50% of the withdrawal sum (capped at $400,000) | |

| Withdrawal in full due to terminal illness | 50% of the full withdrawal sum less an exempt amount of up to $400,000 | |

| In the event of bankruptcy | 100% of the withdrawal sum | |

| Withdrawal in one lump sum by a foreigner (with at least 10 years holding period) | 50% of the lump sum | |

| Early withdrawals before the prescribed retirement age | 100% of the withdrawal sum | Yes |

2) CPF Special Account (CPF SA)

Pros of Putting My Money in CPF SA:

- You are automatically enrolled and start contributing once you start work (if you’re a Singapore citizen or PR)

- You get 4% p.a guaranteed by the Singapore government [The first $60,000 of your combined balances (OA, MA and SA) earns an extra 1% interest per annum]

- You can use it as a ‘bond’ option in your portfolio, where the maturity is at 55 or 65 years old.

Cons of Putting My Money in CPF SA:

- You can only top up a maximum of $16,000 ($8,000 for self-contribution + $8,000 for family members) in cash for tax relief every year up to the Full Retirement Sum for those under 55 and the Enhanced Retirement Sum for those over 55

- note that the annual personal income tax relief cap of $80,000 applies

- This amount of tax relief you can get is also shared with any voluntary contributions you make to your MediSave account.

- You cannot touch the money until you are 55 or 65, even when you really need it.

3) Cash in Bank

Pros of Putting My Money in the Bank:

- You get about 1+% p.a if you have a monthly salary and can fulfil the requirements set by the bank (e.g. credit card spending, bill payment, insurance, etc.)

- You can withdraw the money anytime

- You can decide what you want to do with your money at any time (either to save or invest and earn potentially higher returns).

Cons of Putting My Money in the Bank:

- You don’t get any tax deductions at all

- Your money will lose its value over time since inflation is much higher than 0.05% p.a. if you just hold on to it and don’t invest it.

Step-by-Step Guide To Opening and Topping Up Your SRS Account (2022)

It’s straightforward.

I did it in less than 5 minutes via DBS/POSB’s digibank platform.

Disclaimer: we’re not sponsored; I just decided to open my SRS account with DBS since I have most of my money with them

Step 1: Log in to Your bank’s iBanking website with your User ID and PIN

Complete the Authentication Process.

Step 2: Apply for a Supplementary Retirement Scheme Account

Just follow the instructions, and you should get it opened almost immediately after completing the Authentication Process.

Step 3: Select your Reference Account for Signature, select your Debiting Account and indicate a Contribution Amount.

Step 4: Complete Application

Ensure that your details are updated, check the Acknowledgement and click Next. Verify the details and click Submit to complete the application.

Step 5: Make a $1 Top Up to Your SRS Account

Topping up your SRS account is almost like you’re transferring money from one savings account to another.

It’s really that easy!

And that’s it!

Is It Worth Putting Money In Your SRS Account?

If you’re convinced that an SRS account is helpful for your retirement planning and want to lower your taxes.

You will just need to open up your SRS account.

SRS Promotion 2022

But if you wondering, there are currently no promotions for opening an SRS account with the banks.

So there you have it!

I hope this helps you think about how an SRS account can help your retirement planning.

While lowering your taxes!

If you need help with retirement planning or want to discuss it more with like-minded individuals, head over to Seedly right now!

Related Articles

- Black Friday Sales & Cyber Monday Singapore: Best Deals And Promotions For Shopping, Electronics, and Fashion

- 40 Thoughtful Christmas Gift Ideas That Cost ≤$20 For Secret Santa

- A Singaporean’s Guide to ERP Rates, Gantries & Operating Hours in Singapore

- 12.12 Sales Guide: Best Deals And Promo Codes For Singaporeans

- Best Japanese Buffets: Unlimited Sashimi & Wagyu Beef To Eat Your Money’s Worth

- National Steps Challenge Season 6: Earn up to $85 worth of HPB eVouchers While You Get Healthy!

- The Thrifty Driver’s Ultimate Guide to Free Parking in Singapore

Advertisement