CPF Special Account (SA) Top-Up: A Step-by-Step Guide to Grow Your Retirement Funds & Save on Income Tax

As we were nearing the end of the year, I spent the morning together with my wife, going through our yearly finances, identifying where we could have done better.

Overall, it was pretty satisfactory.

We did grow our savings, investments, and, most importantly, our Central Provident Fund (CPF) as well.

We noticed that one consistent growth was in our CPF accounts.

And that made us pretty happy as it assured us that our retirement funds were growing.

I was then reminded of Mr 1M65, Loo Cheng Chuan, sharing on how you can accelerate your overall savings even faster via the CPF Special Account (SA).

And we decided to practice what was preached.

In fact, CPF reported that despite the challenging economic conditions in 2021, more than 220,000 members topped up more than $4 billion to their own or their loved ones’ retirement savings as of Nov 2021.

Of the CPF members who made top-ups, more than half of them (over 127,000) were first-timers who had either topped up for themselves or for their loved ones.

Thinking of doing the same?

Here’s a step-by-step guide on contributing to your CPF Special Account (CPF-SA) via the Retirement Sum Topping Up Scheme (RSTU).

Note: By the way, we’re not sponsored or paid to write this. Any opinion is purely my own sharing!

TL;DR: CPF Special Account Top-Up Guide — Grow Your CPF Retirement Account Funds & Save on Income Tax

Did you know that topping up your SA will help you to save on your yearly income tax?

However, you should consider this only if you have some spare, liquid cash (between $500 to $8,000 would be a good range) on hand that you won’t need until retirement. Why $8,000? It’s all about tax relief.

From 1 Jan 2022, you will enjoy annual tax relief of:

- Up to $8,000 (previously $7,000) for cash top-ups to your own SA/RA and/or MA*

- And up to $8,000 (previously, $7,000) for cash top-ups to your loved ones’ SA/RA and/or MA*.

This cap is shared between the Retirement Sum Topping-up (RSTU) scheme and voluntary contributions to employees’ MediSave Account (MA).

CPF SA Top-Up Limit: How Much Can I Contribute to SA?

Here are a few things other to take note of:

- Only cash top-ups to the SA/RA within the prevailing FRS ($198,800 in 2023) are eligible for tax relief

- The amount of tax relief you get from RSTU top-ups is limited by the $80,000 annual personal income tax relief cap.

And if you don’t intend to touch it until you’re 65 years old (yes, that’s a damn long time) where it will be streamed out as monthly payments under CPF LIFE.

Can I Top Up My CPF SA? Why Make a CPF Top Up to My Special Account (SA)?

You can

- A Top up to your own and/or loved ones’ Special Account for recipients aged 55 and below, up to the current Full Retirement Sum (FRS). For those aged 55 and above, you can do a top-up to the RA up to the current Enhanced Retirement Sum (ERS)

- Take advantage of compound interest and grow your retirement savings — your $8,000 will become ~$26,553 in 30 years!

- Save on total taxable income by $8,000 for yourself and $8,000 for your loved ones for a total of $16,000.

HOWEVER, this action is irreversible.

If you are keen, it takes about 10 minutes to do this online or via PayNow.

While you can wait till the end of the year to do this, you can also choose to do this cash top-up early in the year!

Before I detail this step-by-step (with pictures).

I want to share more about the ‘magic’ behind compound interest and explain why doing this top-up works for the better…

Click to Teleport

- Top-Up CPF Pros: Compounding With 4% Per Annum Interest Works ‘Magically’

- Top-Up Pros: Top Up Your Parents’ CPF or Your CPF and Save On Your Income Tax

- Cons: You Say Goodbye to Your $8,000 for a Very Long Time

- Should I Top Up CPF SA or MA?

- Step-by-Step Guide To Top Up Your CPF SA

CPF Cash Top-Up Pros: Compounding With 4% Per Annum Interest Works ‘Magically’

If you leave your cash in a regular bank savings account, you’ll get a paltry 0.05% p.a.

If you use a high-interest savings account, you’ll probably get anywhere between 0.05% to 7.88% p.a. if you fulfil all the conditions:

But these interest rates can change at any time at the bank’s discretion.

And what’s even worse is that when you see your cash sitting there… there’s a higher chance that you would spend it.

CPF SA Account Interest and More

However, if you choose to put that cash into your CPF account instead, CPF accounts offer a bonus interest rate of up to 6% p.a., depending on your age and the amount you have in your CPF accounts:

I’m sure some of you might think you can get more than that out there.

But the risk is definitely higher than putting it in your CPF account, which is backed by the AAA-rated government of Singapore.

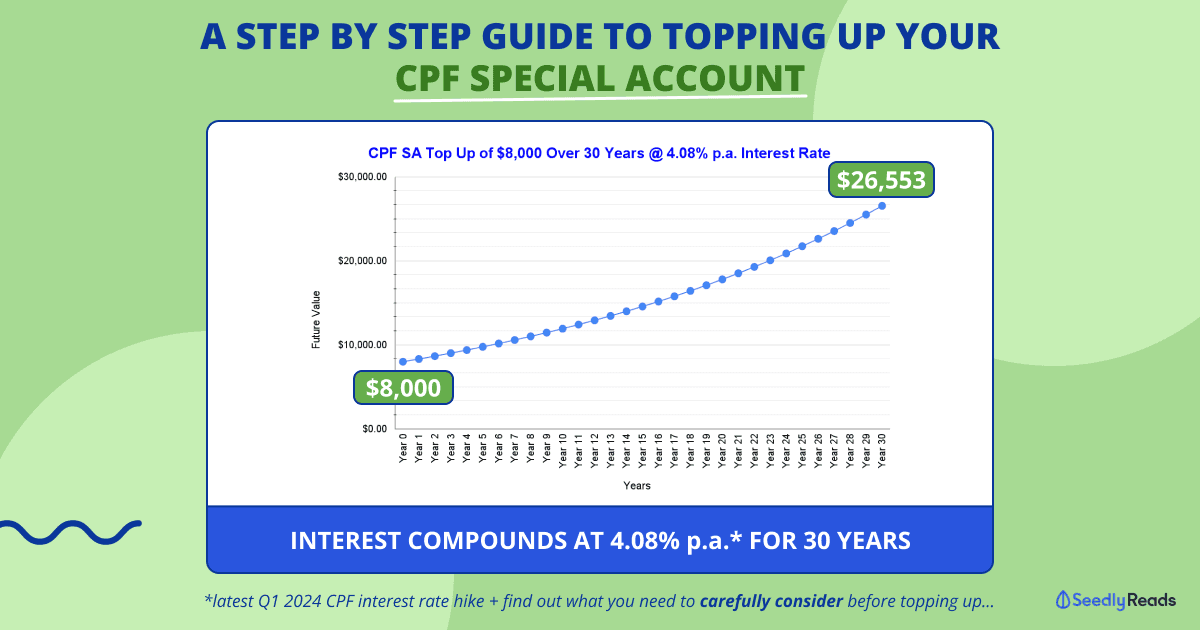

30 Years From Today: Your $8,000 Will Become ~$26,553

So…

“How much will $8,000 be in the future,” you ask?

I did a little math and worked some Excel magic to come up with this chart and table:

| Years | Future Value |

| Year 0 | $8,000.00 |

| Year 1 | $8,326.40 |

| Year 2 | $8,666.12 |

| Year 3 | $9,019.69 |

| Year 4 | $9,387.70 |

| Year 5 | $9,770.72 |

| Year 6 | $10,169.36 |

| Year 7 | $10,584.27 |

| Year 8 | $11,016.11 |

| Year 9 | $11,465.57 |

| Year 10 | $11,933.36 |

| Year 11 | $12,420.24 |

| Year 12 | $12,926.99 |

| Year 13 | $13,454.41 |

| Year 14 | $14,003.35 |

| Year 15 | $14,574.69 |

| Year 16 | $15,169.33 |

| Year 17 | $15,788.24 |

| Year 18 | $16,432.40 |

| Year 19 | $17,102.85 |

| Year 20 | $17,800.64 |

| Year 21 | $18,526.91 |

| Year 22 | $19,282.81 |

| Year 23 | $20,069.54 |

| Year 24 | $20,888.38 |

| Year 25 | $21,740.63 |

| Year 26 | $22,627.65 |

| Year 27 | $23,550.85 |

| Year 28 | $24,511.73 |

| Year 29 | $25,511.81 |

| Year 30 | $26,552.69 |

This chart shows you that if you topped up $8,000 into your CPF SA today.

It’ll grow to become ~$26,553 in 30 years.

If you think about it, that’s really incredible, with an almost risk-free interest rate of 4.08% p.a.

This is based on the latest changes to CPF Interest Rates.

With the Special and MediSave Account (SMA) pegged rate exceeding the floor rate of 4%, savings in the SMA will earn 4.08% in the first quarter of 2024. This is due to the increase in the 12-month average yield of 10-year Singapore Government Securities (10YSGS), which the SMA interest rate is pegged to. In addition, the interest rate for the Retirement Account (RA) will go up to 4.08% for the same time period.

With the Special and MediSave Account (SMA) pegged rate exceeding the floor rate of 4%, savings in the SMA will earn 4.08% in the first quarter of 2024. This is due to the increase in the 12-month average yield of 10-year Singapore Government Securities (10YSGS), which the SMA interest rate is pegged to. In addition, the interest rate for the Retirement Account (RA) will go up to 4.08% for the same time period.

My wife and I are in our late 20s this year.

This means when we turn 65 in about 30-plus years — the value in our CPF SA will definitely be more than three times its current balance just by compounding at 4 % to 5% p.a.

That sounds like a pretty good retirement nest egg.

And potential extra funds for us to leave for the next generation — if we want to.

CPF Self-Contribution Pros: Top Up Your Parents’ CPF or Your CPF and Save On Your Income Tax

By topping up your CPF SA, you can:

- Grow your retirement savings earlier by taking advantage of time and compound interest

- Save on your own taxable income by up to $8,000 a year for individual contribution

- Save another $8,000 in your own taxable annual income by doing a top-up for your spouse, parents, parents-in-law, grandparents, grandparents-in-law, or siblings.

An important thing to take note of as commentator Trevor H pointed out:

Top Up Special Account Cons: You Say Goodbye to Your $8,000 for a Very Long Time

As the Chinese saying goes, “You first taste bitter before you taste sweet”.

This is admittedly a very Asian mentality.

But what I’m trying to get at is that pressing the button to transfer the $8,000 was pretty painful.

Here are the cons of topping up your SA via the RSTU to consider.

These RSTU monies are set aside for your retirement needs and can only be used for monthly payouts under the Retirement Sum Scheme or CPF LIFE.

Any amount topped up to your SA/RA is irreversible and cannot be withdrawn until you reach retirement age. You get a more generous base interest of up 4% – 5% p.a. because your money is put aside for the long term.

For this reason, CPF does not allow you to withdraw RSTU Monies except for your retirement:

Also, CPF states that your SA funds cannot be used for:

- Other CPF schemes for education, investment, insurance, housing, CPF transfers etc.;

- Withdrawals from RA (including property owners); and

- Via exemption from setting aside a retirement sum in the RA.

However, in my opinion, doing this CPF SA top-up is a very prudent decision in the long run.

So, as painful as it was, we’ll definitely do this again next year to grow our CPF Special Account at a compounded rate!

Should I Top Up CPF SA or MA?

Alternatively, you might want to top up your CPF MA instead of your CPF SA. Here’s what you need to consider:

How To Top Up CPF Special Account: A 7 Step Guide To Top Up SA Account

If you’re convinced by what I’ve shared so far.

And want your retirement savings in your CPF SA to grow faster…

Just follow this step-by-step guide to find out how to transfer cash into your CPF Special Account.

All it takes is just 10 minutes of your time.

Note: you can either download the CPF Mobile App or head over to the CPF Website (which I have used)

STEP 1: Navigate to “Tools and Services” on the CPF Home Page

Click on ‘Forms and e-Applications’

Submit an online application via “My Requests” and select “Building Up My / My Recipient’s CPF Savings”.

STEP 2: Click on “Cash top-ups and CPF Transfers for Retirement” Under the “Save More With CPF” Tab

Click ‘”Apply online”.

Read the Disclaimer and click “Start”. and login to your CPF account.

STEP 3: Select Payment Method

The first step would be to select the method of payment. I chose “Cash top-up via PayNow QR” as it is more convenient:

Step 4: Enter Details and Select Recipients of Top-Up

Next would be to enter your details. You will need to select whether you would like to make a top-up to your own account or the accounts of your loved ones and how much you would like to top-up:

STEP 5: Confirm Top-Up

Next, review your details and confirm the top-up.

STEP 6: Make Payment Using Your Selected Payment Method

The second last step would be to process payment using your preferred payment method:

STEP 7: Check That Your Payment Has Been Received

You can check this under the “my cpf” tab located on the CPF home page and click on the “my cpf home” button under the “Latest transactions” header.

Parting Thoughts: You Have to Taste Bitter First Before Enjoying the Sweetness

I’ve shared the pros and cons of topping up your CPF Special Account.

But most importantly, I want to highlight again that this action is IRREVERSIBLE.

Meaning you should only do this if you do not intend to touch the $8,000 for the next 30 to 40 years of your life.

But on the flip side.

The magic of compound interest is really cool, so this is something that you should seriously consider if you’re serious about your retirement.

Alternatively, you can also consider the $1 top-up to your Supplementary Retirement Scheme hack!

Related Articles

Advertisement