Compound Interest: A Ridiculously Easy Way to Get Rich

Let’s get this straight, this is NOT a scam.

And ‘Compound Interest’ is not the name of some multi-level marketing (MLM) scheme that I’m trying to sell you in this article either.

So if you’re looking for that…

Well… look somewhere else.

I am, however, going to let you in on a little secret today.

Whether you’re 25 or 45 years old, did you know that there’s a ridiculously easy way to get rich and retire comfortably?

Yep.

And anyone can do it.

It’s called compound interest.

And it’s what will turn $1,000 a month into $1,522,077 over a span of 40 years.

TL;DR: How to Retire a Millionaire With the Aid of Compound Interest

It’s never too early or too late to use the magic of compound interest to your favour.

But you’re HIGHLY recommended to start early in order to have time on your side.

Even if you’re 40 years old today with no savings… retiring as a millionaire is still within reach.

You just need to put aside a LOT more each month to make it a reality.

So do yourself a favour and start thinking AND doing something about your retirement today.

Why Should I Care About Compound Interest?

Only one in every five Singaporean youth believes that their parents have enough personal savings to finance their retirement.

While only 15 per cent trust that their parents have planned for retirement.

And that they would not have to worry about them in their golden years.

On average, the parents surveyed started to save and plan for retirement at 36 years old.

With the expectation that they will retire at around 63 years old.

Yet a worrying 67 per cent of parents have shared that they expect to outlive their savings.

FYI: Singapore’s average life expectancy is 83 years old.

.

.

.

So how confident are you about your retirement?

Maybe you have just entered the workforce and haven’t even thought about what you’re going to do with your first paycheck.

Or maybe you’ve already got a couple of investments lined up that will (hopefully) see you through your golden years.

But is it enough?

When should you start investing?

And how much should you put aside?

Well, the concept of compound interest states that you should start saving and investing right now.

So… What Is Compound Interest?

Compound interest refers to the interest calculated on the sum of your initial principal and the accumulated interest.

Or more simply, it’s ‘interest on interest’.

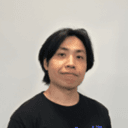

The earlier you allow compound interest to work its magic, the more impressive your long-term results will be.

The chart below shows you how much your savings would have accrued over the years if you started at 25, 35, and even at 40 with twice the savings.

It’s evident that starting at 25 years old seems to be the most logical (and least painful) choice huh?

And if you applied this to your investments.

The earlier you start building and contributing to your investment portfolio, the more money you’ll see by retirement.

How Does Compound Interest Work?

The best way to understand this is by looking at my friends: Jennifer and Samantha.

Both women are childhood friends, who were inseparable since kindergarten.

After completing their degrees at a local university, they started work together at the age of 24.

Both were also fortunate enough to come across a magical mutual fund that promises to be their answer to a comfortable retirement.

As both women actively read Seedly (shameless plug here), they are aware that investing for their retirement is important.

Despite being the best of friends, and having plenty in common…

Jennifer and Samantha DO NOT have experience with investing and never talked about what their plans would be like in order to retire by 62 years old.

Here’s what happens.

“I’m an investment noob but I know that I need to start now!”

Jennifer decides to educate herself by reading our Investment Guide.

She carefully weighs the risk and potential returns of the mutual fund.

And decides that she will start putting $1,000 every month, towards her retirement.

On her 35th birthday, she sees how much her account has grown and decides that she’s going to stop contributing to the fund.

At that point, she has invested a total of $132,000 over a span of 11 years.

“Aiya chill lah… I’m only 24 leh. Looooong way to retirement.”

Samantha is unsure about investing in the mutual fund and decides to sit on it for a while.

The years pass and she never gets around to it, thinking that 62 years old is far away.

When she finally turns 35, the idea of investing for her retirement seems more urgent and “necessary”.

After all, she only has another 27 years to go.

She decides to contribute $1,000 a month to the mutual fund for her retirement.

In fact, she keeps it up till she hits the retirement age of 62.

Now, the two lifelong friends are 62 years old and are looking forward to retirement.

The great news is that after all those years of investing, they’ve both accumulated a sizeable retirement fund.

Before we look at their balance, we’re going to assume a few things here:

- This magical mutual fund is a solid performer that the ladies can hold forever (yes, it’s near impossible to find something like that in the market so suspend your disbelief for a bit yeah?)

- Both women reinvest all of their dividends back into the mutual fund

- They never have to worry about losing their principal

- The fund only gives a modest return of 5% annually AND never makes a loss throughout their lifetime

Note: I know that this is more akin to a ridiculously high-interest savings account, but that it’s even more unlikely that you’ll find one that will give you 5% interest p.a.

| Age | Jennifer's Yearly Contribution | Jennifer's Yearly Balance | Samantha's Yearly Contribution | Samantha's Yearly Balance |

|---|---|---|---|---|

| 24 | $12,000 | $12,600 | $0 | $0 |

| 25 | $12,000 | $25,830 | $0 | $0 |

| 26 | $12,000 | $39,722 | $0 | $0 |

| 27 | $12,000 | $54,308 | $0 | $0 |

| 28 | $12,000 | $69,623 | $0 | $0 |

| 29 | $12,000 | $85,704 | $0 | $0 |

| 30 | $12,000 | $102,589 | $0 | $0 |

| 31 | $12,000 | $120,319 | $0 | $0 |

| 32 | $12,000 | $138,935 | $0 | $0 |

| 33 | $12,000 | $158,481 | $0 | $0 |

| 34 | $12,000 | $179,006 | $0 | $0 |

| 35 | $0 | $187,956 | $12,000 | $12,600 |

| 36 | $0 | $197,354 | $12,000 | $25,830 |

| 37 | $0 | $207,222 | $12,000 | $39,722 |

| 38 | $0 | $217,583 | $12,000 | $54,308 |

| 39 | $0 | $228,462 | $12,000 | $69,623 |

| 40 | $0 | $239,885 | $12,000 | $85,704 |

| 41 | $0 | $251,879 | $12,000 | $102,589 |

| 42 | $0 | $264,473 | $12,000 | $120,319 |

| 43 | $0 | $277,697 | $12,000 | $138,935 |

| 44 | $0 | $291,582 | $12,000 | $158,481 |

| 45 | $0 | $306,161 | $12,000 | $179,006 |

| 46 | $0 | $321,469 | $12,000 | $200,556 |

| 47 | $0 | $337,543 | $12,000 | $223,184 |

| 48 | $0 | $354,420 | $12,000 | $246,943 |

| 49 | $0 | $372,141 | $12,000 | $271,890 |

| 50 | $0 | $390,748 | $12,000 | $298,084 |

| 51 | $0 | $410,285 | $12,000 | $325,589 |

| 52 | $0 | $430,799 | $12,000 | $354,468 |

| 53 | $0 | $452,339 | $12,000 | $384,791 |

| 54 | $0 | $474,956 | $12,000 | $416,631 |

| 55 | $0 | $498,794 | $12,000 | $450,063 |

| 56 | $0 | $523,639 | $12,000 | $485,166 |

| 57 | $0 | $549,821 | $12,000 | $522,024 |

| 58 | $0 | $577,312 | $12,000 | $560,725 |

| 59 | $0 | $606,178 | $12,000 | $601,361 |

| 60 | $0 | $636,487 | $12,000 | $644,030 |

| 61 | $0 | $668,311 | $12,000 | $688,831 |

| 62 | $0 | $701,727 | $12,000 | $735,873 |

Jennifer invested a total of $132,000 for the first 11 years, which eventually grew to $701,727.

Samantha, who started a little later, invested a grand total of $336,000, which doubled to $735,873 by her 62nd birthday.

If you do the math…

You’ll notice that since Samantha started later, she had to put in 2.5 times more money than Jennifer did.

And she only came out $34,146 ahead.

Jennifer, on the other hand, grew her principal by more than 5 times.

Yep.

That’s the magic of…

While both Jennifer and Samantha were blessed with an almost magical mutual fund that enjoyed a relatively modest growth over the course of their investment journey.

Jennifer had the advantage of time.

And because of the compounding effect of interest over time, her money eventually took on a life of its own and continued to grow without Jennifer having to contribute a single cent.

Now, if Jennifer decided to continue her contributions from her 35th birthday all the way till she turned 62…

She would’ve accumulated a whopping $1,522,077.

That works out to be $6,342 a month for the next 20 years of her retirement.

Compound Interest: The Secret’s Out

You’ve seen firsthand how time and compound interest gave Jennifer a HUGE advantage over Samantha.

So if you think that you can wait till you’re 35 before you start getting serious about saving and investing for retirement.

Think about how much you’re missing out just because you decided to chill lah.

Even if you’re 35 or 45 now, it’s not too late to start your retirement investing journey.

Whether you decide to open a Regular Shares Savings Plan or want to go with an online brokerage.

Do yourself a favour and start NOW.

Related Articles

Advertisement