Looking for low-risk investments to park your money and grow your savings?

Whether you’re new to investing or seeking shelter in low-risk investments from the volatile stock market, here are some of the safest, low-risk investments in Singapore for you to park your money!

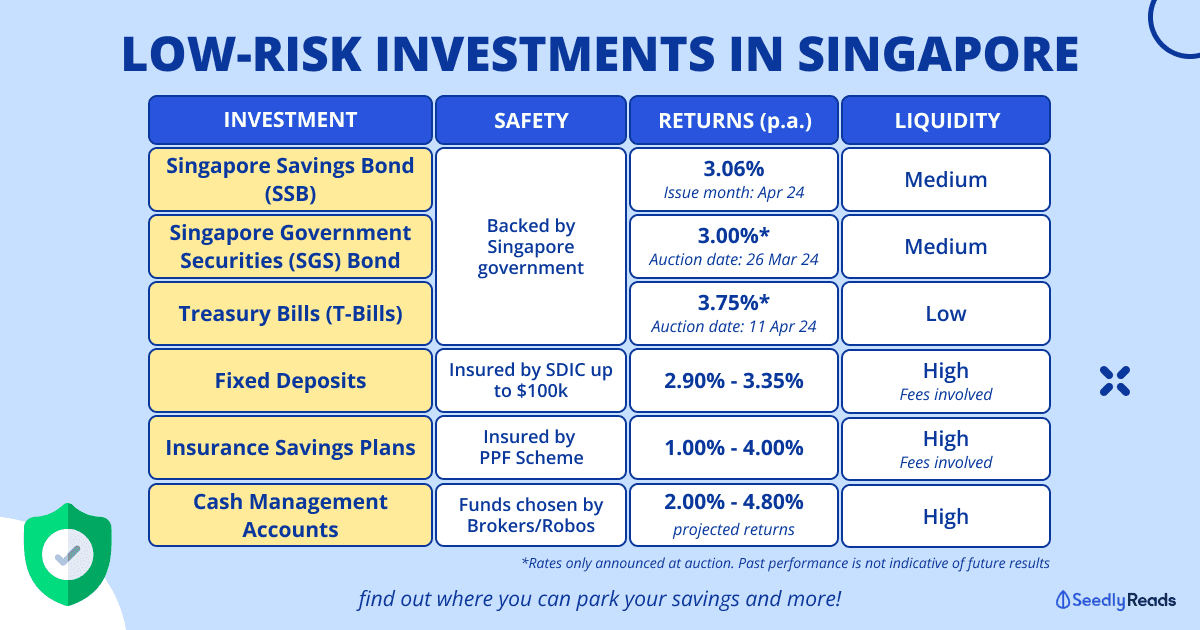

TL;DR: Low-Risk Investments in Singapore to Grow Your Money

| Investment Vehicle | Safety | Returns | Liquidity | Tenor |

|---|---|---|---|---|

| Singapore Savings Bond (SSB) | Backed by Singapore government with "AAA" credit rating | Apr 2024: 3.06% p.a. | Medium | 10 years |

| Singapore Government Securities (SGS) Bond | Last (Auction date: 26 Mar 2024): 3.00% p.a. | Medium (might be a hassle) | 2 to 30 years | |

| Treasury Bills (T-Bills) | Last 6-month T-bill (Auction date: 11 Apr 2024): 3.75% p.a. Last 1-year T-bill (Auction date: 18 Apr 2024): 3.58% p.a. | Low | 6 months or 1 year | |

| Fixed Deposits | Funds insured by SDIC (up to $100,000) | Apr 2024: 2.90% - 3.35% p.a. (promo rates) | High (but with fees) | 2 to 18 months |

| Insurance Savings Plans | Funds insured Policy Owners’ Protection (PPF) Scheme, which has different caps on the amount insured depending on the nature of the insurance plan | 1.00% - 4.00% p.a. | High (but with some fees) | None or 1 to 5 years |

| Cash Management Accounts | Managed by MAS-licensed roboadvisors/digital wealth services/brokers | 2.00% - 4.80% p.a. (Returns are projected and NOT guaranteed) | High | None |

With interest rates skyrocketing and an ever-competitive fixed deposit rate environment, here are our recommended low-risk options for you to grow your savings!

Jump to:

- Singapore Savings Bond (SSB)

- Singapore Government Securities (SGS) Bond

- Treasury Bills (T-bills)

- Fixed Deposits

- Insurance Savings Plans

- Cash Management Accounts

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any investment products.

Singapore Government Securities

First up, we have the Singapore Government Securities, consisting of the Singapore Savings Bond (SSB), Singapore Government Securities (SGS) bonds and Treasury Bills (T-bills).

These securities are completely backed by the Singapore Government, which has a “AAA” credit rating. This reduces the risks of investing in SGS bonds to the bare minimum (read: there’re still risks tho).

Singapore is one of only 11 countries in the world that enjoy the “AAA” credit rating! Some other countries include Switzerland, Australia, and Finland.

Having such a strong rating arguably makes the SGS some of the safest products in the market.

Singapore Savings Bond (SSB)

Perhaps the most popular of the bunch, SSBs have become a much more attractive option for many Singaporeans since interest rates rose.

Aside from its ultra-low risk, investors can lock in interest rates for a decade! Early redemption is also possible and fairly simple if you don’t want to wait for the whole 10 years.

The downsides are that withdrawal can take a while (up to a month) since redemptions are processed by the second business day of the following month and that there are limits to how much you can invest during each round.

Click in for a more in-depth look at how to invest in SSBs:

Singapore Government Securities (SGS) Bonds

Another option to consider is SGS bonds. It features the same backing from the Singapore government with varying tenors of 2 – 30 years.

While they can be more liquid than SSBs, you may find it a hassle to sell SGS bonds on the secondary market, which is thus unsuitable for beginners. Moreover, the interest rates are only determined during the auction date. Nonetheless, if you’re fine with parking your money for the specified tenor, you can reap the high interest!

If you’re still interested in how SGS Bonds work, click in for a more in-depth look at how to invest in SGS Bonds.

Treasury Bills (T-bills)

Lastly, we have T-bills, a “hidden gem” that many Singaporeans used to overlook. Like SSB and SGS bonds, these are ultra-low risk investments with a short tenor of either 6 months or a year, with 6-month T-bills being the most common. The best part? The latest interest rates are 3.75% p.a. (auction date: 11 Apr 2024) for the 6-month T-bill and 3.58% p.a. (auction date: 18 Apr 2024) for the 1-year T-bill!

This beats the majority of fixed deposits, and you don’t have to queue at a bank to apply either.

That said, T-bills are rather illiquid even though they can be sold in the secondary markets, and their interest rates are not announced until the auction date itself.

Click in for a more in-depth look at how to invest in T-bills:

Singapore Deposit Insurance Corporation (SDIC) Insured Investments

Next, we have SDIC-insured investments where SDIC will reimburse your investments of up to $100,000 in the CPF Investment Account with the bank, in case the bank goes under. These are also ultra-low-risk investments with an extra layer of protection just in case.

Fixed Deposits (FDs)

Not so keen on dealing with investment limits, and uncertain interest rates? Traditional fixed deposits are still a great and safe way to go, especially with all the banks rapidly increasing their interest rates in the past few months.

FDs are also very liquid as you can withdraw them at any time. However, you will have to eat some harsh early withdrawal fees of 0.5% – 1.0% p.a. of the sum you’ve invested. Lastly, depending on the bank, you’ll need to hit much higher minimum investment amounts of $5,000 or more.

Click in to look at what the banks are currently offering:

Insurance Savings Plans

Insurance Savings Plans can be a great option for you to consider if you want more liquidity in case of emergencies and some insurance coverage. They are insured under the Policy Owners’ Protection Scheme, which has different caps on the amount insured depending on the nature of the insurance plan.

P.S. The Singlife account got an upgrade; up to 4% p.a. now!

Click in for a more in-depth look at Insurance Savings Plans.

Cash Management Accounts

If you want an all-rounder in terms of liquidity and low risk, cash management accounts are a great choice to help you invest in money market funds.

That said, these are not backed by the Singapore government or SDIC-insured.

Unlike the others listed above, the returns stated are only projected and NOT guaranteed. So there is a chance that you could suffer losses in your investment.

Click in for a more in-depth look at cash management accounts.

Afterthoughts

Low-risk investments may not offer the excitement of high returns in the stock market, but they are a steady and safe way to grow your money, especially during times with high inflation.

While the returns here won’t beat inflation, it’s definitely better than nothing!

If you’re new to investing, the above-listed options are also a perfect way to dip your toes into the world of investing.

But while all of these are low-risk, remember that there ARE still risks involved, as with anything related to investing. As always, be sure to do your own due diligence and read up on the investment vehicles listed here by clicking on the relevant articles to find out more.

If you need a piece of professional advice on your risk profile, you can always seek the services of a professional. This means finding a financial consultant or advisor who is an expert in this area.

Talk to a few of them, determine your needs, balance the recommendations of different consultants, and decide if you want to do it yourself.

Manulife is now offering free consultation for those who are interested to earn passive income but might not feel confident doing so. Check them out below!

Related Articles:

Advertisement