Coast FIRE (Financial Independence Retire Early) in Singapore: Here's How to Secure Your Retirement Early

Joel Koh

Joel Koh●

As much as there’s beauty in work, I would hazard a guess to say that no one wants to get stuck in the rat race until you are old and wrinkled.

This is probably why the Financial Independence Retire Early (FIRE) movement has its fair share of devotees.

For the uninitiated, the FIRE movement is a strategy where you have to aggressively save and passively invest to achieve financial independence and retire early.

Those seeking to attain full-fat FIRE intentionally maximise their savings rate by finding ways to increase income or decrease expenses.

The objective is to accumulate assets until the resulting passive income provides enough money for living expenses in perpetuity. (until you die)

Upon reaching financial independence, paid work becomes optional, allowing for retirement from traditional work decades earlier than the standard retirement age (i.e. between 40 to 50 years old).

But, the full-fat version of fire that we wrote about previously is a daunting prospect, as you will likely have to accumulate a huge investment portfolio just to leave your day job.

Achieving that would require a tremendous amount of hard work, sacrifice and living a very frugal lifestyle. This may not be suited for everyone.

But like how bubble tea has different sugar levels, FIRE has different levels of intensity as well.

You don’t have to go all-in and reach for 0% sugar (full-fat fire strategy). There are other more attainable FIRE strategies like the Barista FIRE and Coast FIRE strategies which may be more achievable for most.

Speaking of Coast FIRE, this is the strategy I am currently employing and working towards.

Intrigued?

Here is what you need to know!

TL;DR: How to Coast FIRE (Financial Independence Retire Early) In Singapore

- Well Coast FIRE refers to the strategy of saving and investing enough to guarantee a comfortable retirement at your planned retirement age (e.g. Singapore’s official retirement age is 62 in 2021) ahead of time.

- Achieving Coast FIRE is liberating, more attainable than full fat fire and would grant you more job autonomy.

- Also, use the linked calculator to figure out how much you need to achieve your personal Coast FIRE milestone.

Disclaimer: The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any investment product.

What is Coast FIRE?

I have chosen to employ the Coast FIRE strategy as it is the most straightforward. Plus, I enjoy what I’m doing at work, spending money (within reason), and I’m not entirely sure what I will do if I retire as well.

But what is Coast FIRE, you may ask?

Well Coast FIRE refers to the strategy of saving and investing enough to guarantee a comfortable retirement at your planned retirement age (e.g. Singapore’s official retirement age is 62 in 2021) ahead of time.

After that, you leave your investments to compound so you can “coast”. Do note that you cannot touch the money you are saving and investing for retirement for this to work.

After achieving your Coast FIRE financial goal, you can choose to stop saving and investing for retirement, and from this point onwards, you just need enough income to cover your expenses.

Although you won’t be able to retire early, you can rest assured in the knowledge that your retirement is secured.

Coast FIRE Benefits

Achieving Coast FIRE has a few key benefits.

Achieving Coast FIRE Is Liberating

Once you hit your Coast Fire financial goal, you get a true sense of relief in the assurance that you will have a comfortable retirement once you reach that age.

This safety net will allow you to take risks in life.

Achieving Coast FIRE Is More Attainable

Although you won’t be able to retire early, achieving Coast FIRE is a lot more attainable compared to a full-fat FIRE.

Although achieving financial independence and retiring early is great, having to save 80 per cent of your salary to retire at 40 may not be the best option for most and downright impossible for some.

As achieving Coast FIRE is more attainable, there is also a psychological benefit.

When people see that a goal is more attainable, they are more likely to stick to it.

Achieving Coast FIRE Will Give You More Job Autonomy

For many, achieving your Coast FIRE milestone, you have the freedom to change jobs for something less stressful and more enjoyable.

You could shift to part-time jobs or freelance work and spend more time and money on things that truly matter to you.

Another option will be to continue saving and investing for retirement. This will let you retire with more cash or even retire early.

In a sense, Coast FIRE could be a gateway drug to full-fat fire.

How to Achieve Coast Fire

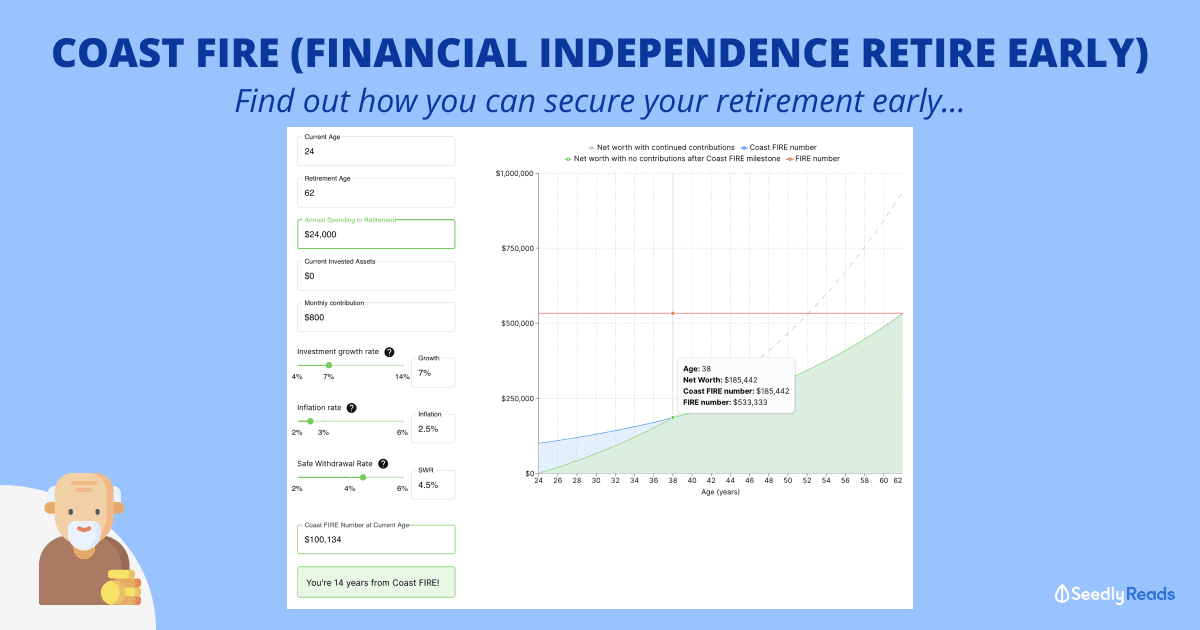

To help you figure out how much you need to Coast FIRE, I will be using this excellent calculator made by Andrew, the author of WalletBurst.

Here are a couple of Andrew’s assumptions that I have localised:

- ‘On the left, start by entering your current age and the age you plan to retire.

- Then enter the amount you plan to spend annually in retirement.

- In the Current Invested Assets box, enter the amount that you currently have invested. For example, if you have S$100,000 invested in the stock market and S$25,000 saved in your emergency fund, then you should enter S$100,000 in this field.

- Use the sliders to adjust the rates and watch the graph to the right immediately react to your change!

- The investment rate of return is the average return you expect your investments to grow, not adjusted for inflation.

- This calculator uses 7% as a default Investment rate of return, a relatively conservative assumption. Historically, the S&P 500 has returned on average 10% annually from its inception in 1926 to 2018.

- Inflation rate is the average annual rate of inflation that you expect to experience in the future. Historically, Singapore’s average inflation rate from 1962 – 2021 stands at 2.5 per cent (via Trading Economics).

- Safe Withdrawal Rate (SWR) is the estimated percentage of your net worth that you expect to withdraw to cover your living expenses in retirement. 4% is widely considered as the recommended SWR for retirement planning. This 4% withdrawal rate was found by the Trinity Study to have a 100% success rate over a 30-year retirement horizon with a 50% / 50% mix of stocks and bonds.

- But in a January 2021 interview with Barrons, William Bengen, creator of the 4% withdrawal rate study has updated his research to suggest investors could withdraw 4.5% annually safely. You can read about it here.

- In Singapore, the average life expectancy for residents is 83.9 years old. If you retire at 62, you are looking at a traditional 22-year retirement. This means that the estimate you get is more generous, which will help account for any uncertainties in life that come your way.

- Illustrative profile of Calmond, a 24-year-old fresh graduate who has just started working.’

- Calmond has:

- No savings but has put aside six months of expenses in his emergency fund.

- Can put aside S$800 a month to invest.

- Plans to retire at the age of 62.

- Want to have a retirement income of S$2,000 a month.

Let’s break it down further.

To achieve Coast FIRE, Calmond will have to work for about 14 years till age 38 and contribute $800 a month consistently till then.

By 38, Calmond would have a net worth of S$185,442 in his retirement fund.

From this point onwards, Calmond will just have to stay invested, not withdraw anything from his retirement fund until age 62 and let compounding do its magic.

He will not have to invest anything else from this point and still retire comfortably.

After hitting his planned retirement age, he can safely withdraw about 4.5% of his retirement portfolio every year.

This is easier said than done.

But, as everyone’s personal financial situation is different, feel free to play around with the calculator to estimate how much you need.

Also in Singapore, there are two magical things that happen to you in your later stage in life if you are a salaried working adult who is fortunate enough to receive Central Provident Fund (CPF) contributions while working:

- Age 55: Your CPF Retirement Account (RA) will be created and you would be able to withdraw amounts in your CPF above your Basic Retirement Sum OR Full Retirement Sum.

- Age 65: Your CPF LIFE will kick in, giving you additional monthly payouts of between $500 to more than $2,000 depending on the amount in your Retirement account.

You can factor these in as well when you do your planning.

Closing Thoughts

Here is some additional food for thought.

Previously our founder Kenneth Lou chatted, wrote this Singapore FIRE guide and talked to Kyith from Investment Moats, one of Singapore’s first financial bloggers.

Kyith gave him some excellent perspectives about FIRE to share with our readers.

Looking at the simple formula below…

You just need to do two out of three of these well:

- EARN: How you can seek higher increments and bonuses to achieve a higher income level.

- SAVE: This is obviously very important, as described above, how you can find ways to increase your savings rate (or conversely, reduce your expenses monthly).

- INVEST: This is one of the ways to shortcut your FIRE journey if you can achieve more returns on your money, making it work harder for you.

If you are new to investing, do read our beginner’s four-step checklist before starting your first investment and our ultimate guide to investing in Singapore before you begin your journey!

With that, I wish you all the best in your FIRE journey.

Advertisement