Property Cooling Measures in Singapore & How They Affect a Resale Homeowner

The Housing Development Board (HDB), Ministry of National Development (MND) and Monetary Authority of Singapore (MAS) have announced that starting from 30 September 2022, a slew of property cooling measures will be rolled out to fan off the heat from the resale market.

Very quickly, these measures are:

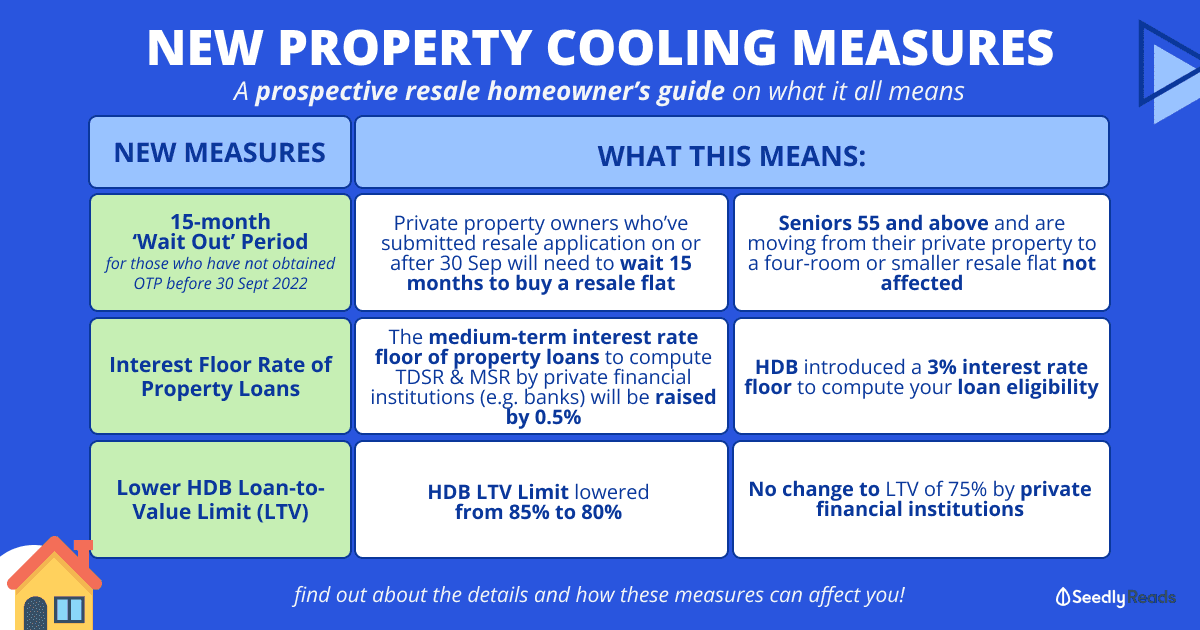

- A new 15-month ‘wait out’ for private property owners after selling their property before they can buy a non-subsidised HDB resale flat

- The loan-to-value (LTV) limit for HDB loans will also be lowered from 85 per cent to 80 per cent

- Changes to the interest rate floor of property loans by private financial institutions and HDB will introduce a 3% interest rate floor for computing eligible loan amount

Let’s take a deeper dive into what each policy change would mean for Singaporean resale home buyers!

TL;DR: HDB Property Cooling Measures for Resale Houses

Click here to jump:

- 15-month wait-out period for private homeowners

- Interest rate floors of private financial institutions and HDB

- Lower HDB Loan-to-Value (LTV) limit

15-month Wait Out Period For Private Property Owners

The Government will impose a wait-out period of 15 months for private residential property owners and those who had disposed of a private property prior to submitting an application to buy a resale flat, to buy a non-subsidised HDB resale flat.

Before 30 Sep 2022, private property owners who sell their private properties within six months of purchasing an HDB flat can buy an HDB resale flat on the open market.

Now, this will no longer be allowed.

So, this means that if you had exercised your Option to Purchase (OTP) before 30 Sept 2022, you have to wait 15 months in order to purchase a resale flat? What if you’ve already sold your private property?

Well, HDB will exercise flexibility such that those who have proof that they’ve obtained an Option to Purchase an HDB resale flat before 30 Sep, they might get the 15-month wait-out period waived.

What you need to do is to submit an appeal to HDB with these documents:

- Proof of payment of the Option Fee (Option fee of $1 to $1,000 in cash is paid to the seller to ‘reserve’ the property) OR

- Proof of payment of Option Exercise fee (Within the option period of 21 days, the buyer can exercise his option to purchase, which means he has legally agreed to buy the flat, and this fee should not exceed $5,000 when the Option Fee is included. Once the option has been exercised, the buyer has legally agreed to purchase the property and cannot back out from the property transaction)

However, in cases where the OTP has NOT been obtained before 30 Sep, but resale buyers have committed to selling or have sold their existing private property, HDB will assess on a case-by-case basis.

In instances where the resale flat buyers are no longer eligible for the purchase due to the 15-month wait-out period, the OTP will become null and void. In these cases, sellers will have to refund the Option Fee paid to the buyer.

Do note that this measure will NOT BE APPLIED to seniors who are 55 and above and are moving from their private property to a four-room or smaller resale flat.

The wait-out period for private property owners who are first-timers and wish to apply for the CPF Housing Grant and Enhanced CPF Housing Grant for their resale flat purchase remains unchanged at 30 months.

That said, the Government has emphasised that this is a temporary measure which will be reviewed in the future depending on overall market conditions and housing demand.

“Since the government implemented a broad package of measures in December 2021, the HDB Resale Price Index has increased by more than 5 per cent as at end-Q2 2022, reflecting a broad-based increase in public housing demand. Given the clear upward momentum in HDB resale prices, MND and HDB will introduce a wait-out period of 15 months for private residential property owners (PPOs) and exPPOs to buy a non-subsidised HDB resale flat as a temporary measure to moderate demand and ensure that resale flats remain affordable for flat buyers, especially for first-timers.”

Changes to Interest Rate Floor

For those who’re keen to take up property loans by banks and other private financial institutions, the MAS will raise the medium-term interest rate floor that’s used to compute the Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR) by 0.5%.

| Type of Loan | Medium-term Interest Rate |

|---|---|

| Residential property purchase loans and mortgage equity withdrawal loans | The higher of a 4% per annum (p.a.) floor (up from 3.5% p.a.) or the thereafter interest rate* |

| Non-residential property purchase loans and mortgage equity withdrawal loans | The higher of a 5% p.a. floor (up from 4.5% p.a.) or the thereafter interest rate* |

| *The thereafter interest rate is the highest possible interest rate applicable during the tenure of a property loan, excluding introductory or promotional rates | |

What implications would this have?

According to the authorities, mortgage interest rates pegged to the three-month Compounded Singapore Overnight Rate Average (SORA) have been rising in the past few months, and will likely increase further in 2023 along with US interest rates, before settling at a higher level compared to the lows from 2013 to 2021.

The revised medium-term rate floors are said to help ensure that homeowners are borrowing prudently for their purchases in a higher interest rate environment, and choose a loan size that’s appropriate for them to service, especially when interest rates are rising.

The higher rate floor will apply across all property loans, not just home loans.

Do note that the actual interest rates charged for mortgages will continue to be determined by your borrower.

This change applies:

- For loans where the Option to Purchase (OTP) is granted on or after 30 September 2022, or where there is no OTP, the date of the Sale and Purchase Agreement is on or after 30 September 2022

- New mortgage equity withdrawal loan applications made on or after 30 September 2022.

- Those refinancing other types of property loans will be subject to the prevailing medium-term interest rate that applied when they first took up their loans. Borrowers who are refinancing owner-occupied property loans will not be affected by this change.

Similarly, stricter criteria will also apply when assessing housing board flat buyers’ eligibility for an HDB concessionary housing loan.

HDB Interest Rate Floor

For those who’re keen on taking up the HDB home loan, the statutory board has introduced a 3% interest rate floor for computing eligible loan amounts.

What implications would this have?

This means that the interest rate used to compute the eligible loan amount for HDB’s concessionary housing loan will be the higher of 3 per cent per annum, or 0.1 per cent above the prevailing CPF Ordinary Account (OA) interest rate, which is currently at 2.5%.

So, in summary, the interest rate floor of 3% applies to:

- flat buyers who are taking an HDB housing loan at the concessionary interest rate; and

- whereby the commercial interest rate is charged, e.g. flat buyers who are taking a second HDB housing loan and buying an HDB flat before disposing of their existing one. The interest rate will be converted to the concessionary rate after the flat buyer has disposed of the existing flat and used the CPF refund and 50% of the cash proceeds received to reduce the second HDB housing loan amount.

In addition, this will only apply to fresh applications for an HDB Loan Eligibility (HLE) Letter received on or after 30 September 2022, 00:00.

This will not affect the actual HDB concessionary interest rate, which will remain unchanged at 2.6% p.a. from 1 October to 31 December 2022.

The interest rate floor to compute the eligible loan amount will take effect as follows:

| Transaction Type | Effective Date |

|---|---|

| Purchase of flats from HDB in Build-To-Order and Sale of Balance Flats exercises | - Application for an HLE letter received; and - Sales launch date On or after 30 Sep 2022, 00:00hr |

| Purchase of resale flats on the open market and open booking flats from HDB | HLE letter application received on or after 30 Sep 2022, 00:00hr |

| Taking over of ownership of existing flat | HLE letter application received on or after 30 Sep 2022, 00:00hr |

Read more:

- Are Resale Flats ALWAYS More Expensive Than BTO Flats?

- Is the HDB Resale Flat Market Overheating?

- The Seedly HDB Resale Guide: Your Ultimate Step-by-Step Guide to HDB Resale Application

Lower HDB Loan-to-Value Limit

Next, the Loan-to-Value (LTV) for HDB housing loans will be lowered from 85 per cent to 80 per cent.

This is a further tightening of the LTV limit for loans from HDB from 90 per cent to 85 per cent last December, to 80 per cent this round.

The lower LTV limit will apply to new flat applications and resale applications on or after Sept 30.

While first-time HDB buyers and lower-income flat buyers may receive more housing grants when buying a subsidised flat directly from HDB, or up to $160,000 when buying a resale flat, or tap on their CPF savings to pay for the flat purchase, thereby reducing the loan amount they may need to take.

This means that you would also need to fork out more cash upfront if you’re not using your CPF.

This revised LTV limit does not apply to loans granted by private financial institutions (e.g. banks), for which the LTV limit remains at 75%.

Read more:

- The Definitive Guide To Updates To CPF Usage And HDB Housing Loan

- Is Your HDB Flat Potentially Worth $0?

How Effective Would These Measures Be?

Last December, the Government announced that Additional Buyer’s Stamp Duty (ABSD) rates will be raised, the Total Debt Servicing Ratio (TDSR) threshold will be tightened, and a lowering of the LTV limit in view of rising resale and private property prices.

However, according to the joint statement released by the authorities, the HDB Resale Price Index has increased by more than 5 per cent as of the end of the second quarter of 2022, which shows that there is a broad-based increase in public housing demand.

So, the previous measures didn’t seem to have worked effectively, hence the new measures are rolled out to cool off the property market even further.

What are your thoughts on these changes?

Share them with us in the Seedly Community’s ‘Property’ group today!

Related Articles:

- Home Loans: Should You Lock In Current Rates Before They Rise Further?

- Shorter vs Longer Home Loan Tenure: What Is Best For You?

- Protect Your Loved Ones From Home Loan Debt: Home Protection Scheme (HPS) Vs Private Mortgage Insurance vs Term Life Insurance

- Is Wiping Out Your CPF To Buy Your First Home A Wise Choice?

- Do You Get All Your Money From Your HDB Sales Proceeds For Your Retirement?

Advertisement