Protect Your Loved Ones From Home Loan Debt: Home Protection Scheme (HPS) Vs Private Mortgage Insurance vs Term Life Insurance

Joel Koh

Joel Koh●

As Benjamin Franklin one of the founding fathers of the United States once said:

but in this world nothing can be said to be certain, except death and taxes.

Old Ben has a point. On top of having to pay taxes, we have really no control over unfortunate events that might result in death.

This is something to keep in mind when you become a homeowner and take on a home loan for your house.

In the unfortunate event that you pass away during your home loan tenure, the burden of the home loan would fall on their loved ones.

Also, as your home is being used as collateral, the bank has the right to foreclose your home while HDB has the right to confiscate your flat if your home loan instalments have not been repaid for an extended period of time.

And if it’s a home you and your family are living in, it also means you will lose the roof over your heads.

If you don’t want this to happen, you can consider buying either the Home Protection Scheme (HPS), private mortgage insurance or term life insurance to protect you and your family.

But you might be thinking. Which option is better for you?

We got you fam!

Disclaimer: Any information provided by Seedly is only educational and is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice or recommendation of any sort offered or endorsed by Seedly or any company. Do seek the advice of a trusted licensed advisor that you trust to help you make objective comparisons.

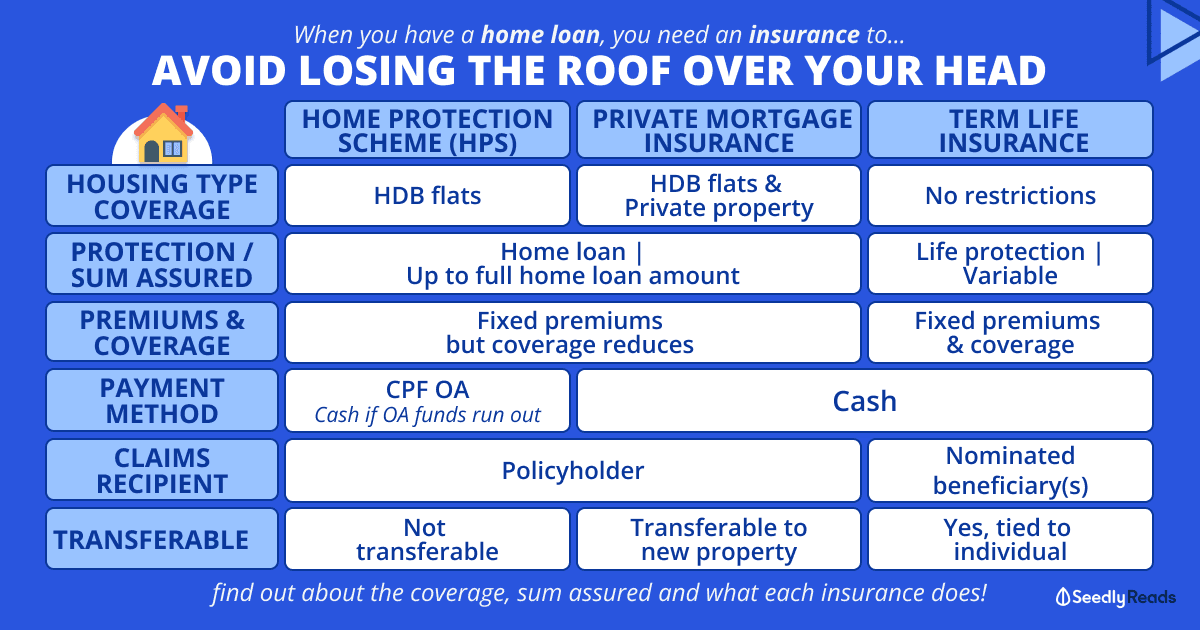

TL;DR: Home Protection Scheme vs Private Mortgage Insurance vs Term Insurance

| Factors | Home Protection Scheme (HPS) | Mortgage Insurance | Term Life Insurance |

|---|---|---|---|

| Housing Coverage | HDB flats | HDB flats & Private property | Can cover HDB flats & Private property |

| Protection | Sum Assured | Home loan | Up to home loan amount | Life protection Variable (up to profile & insurer limits) |

|

| Premiums & Coverage | Fixed/Level premiums but coverage reduces | Fixed/Level premiums and coverage | |

| Payment Method | CPF OA (Can use cash if CPF OA funds run out) | Cash | |

| Claims recipient | Policyholder | Nominated beneficiarie(s) | |

| Transferrable | Not transferrable as HPS is tied to HDB flat | Private mortgage insurance can be transferred to new property | Coverage is tied to the individual and not the property |

| Add-On Benefits | - | Can add riders for critical illnesses, premium waivers, etc. | |

| Cost (Approximate) | $$ | $ | $$$ |

Click here to jump:

- What is home protection scheme?

- What is mortgage insurance?

- What is the best mortgage insurance plan?

- Best term-life insurance that covers home loans

Disclaimer: The Information provided by Seedly does not constitute an offer or solicitation to buy or sell any insurance product(s). It does not take into account the specific objectives or particular needs of any person. We strongly advise you to seek advice from a licensed insurance professional before purchasing any insurance products and/or services.

What is The Home Protection Scheme (HPS)?

Basically, the HPS is a Mortgage Reducing Term Assurance (MRTA) policy that safeguards members and their families against losing their HDB flat in the unfortunate event of death, terminal illness or total permanent disability.

In other words, the payout you receive from this policy will decrease as you repay more of your loan while the premium stays the same.

The Government has made it mandatory for homeowners who use their Central Provident Fund (CPF) savings to service their monthly home loan instalments on their Housing and Development (HDB) flat to be insured under the HPS.

Also, HPS applies to you regardless of whether you are on an HDB or bank home loan.

Should any of these things happen to HPS members, CPF will cover the outstanding amount on their home loan up to the age of 65 or until the home loan is fully repaid, whichever is earlier.

Benefits of the policy will be paid out to the policy owner which could be the bank or the insured person.

However, the HPS cannot cover private residential properties, like privatised Housing and Urban Development Company (HUDC) flats, executive condominiums (ECs) and more.

Also, according to CPF, your HPS cover starts when you meet all of the following conditions:

- You are the legal owner of the flat

- You have completed the loan application with HDB or the approved mortgagee and are now legally responsible for the loan

- You have made your health declaration which is accepted for HPS coverage

- You have paid the first HPS premium.

Here are the pros and cons of this type of policy:

Pros

- CPF Ordinary Account (OA): can use your CPF Ordinary Account (OA) funds to pay for the HPS. (Do take note of the accrued interest on your CPF OA funds)

Cons:

- Limited scope: only for HDB flat owners who are servicing their home loans using their CPF OA funds

- Tied to the HDB flat: once the specific HDB flat is sold, the HPS coverage will be terminated

- Not the cheapest: HPS is generally more expensive compared to private mortgage insurance especially when you are younger.

However, you can apply to be exempted from the HPS if you have any of the following policies:

- Whole Life

- Term Life

- Endowments

- Life Riders (must be attached to a basic policy)

- Mortgage Reducing Term Assurance (MRTA) / Decreasing Term Rider

Is The HPS Premium Fixed?

Thankfully, you can use CPF’s premium calculator to gauge how much you need to pay.

The premium is paid annually and will automatically be deducted from your CPF OA. You will only need to pay the annual premium for 90% of the HPS cover period. The premium is also not fixed and you can adjust your HPS cover according to your share of responsibility in repaying the loan (using your CPF savings and/or cash).

The total share of cover per household must add up to at least 100%. However, you and your co-owner(s) can also each choose to insure for a higher share of cover, up to 100% share of cover

per owner.

When you make a claim, HPS pays the sum assured based on the share of cover that you have applied for. A higher share of cover will result in a higher annual premium which is deducted

from your CPF OA.

It’s important for all homeowners to consider your needs for financial protection and future retirement needs.

Will HPS Get Terminated?

There are two scenarios where your HPS cover can be terminated.

Sell Your HDB flat

Your HPS cover will end when you sell your flat and any unused portion of your premium will be paid into your CPF OA.

This will be applicable to both downsizing and buying a resale flat. If you buy a new flat, the HPS cover for your old flat will end while an HPS cover will be issued for your new flat.

Full Redemption of Housing Loan

Your HPS cover will end when you have fully redeemed your loan, and the unused portion of your annual premium will be paid into your CPF OA.

How Do You Get Exempted From Home Protection Scheme?

Well, these policies would cover your outstanding housing loan, either up to age 65 or until the full term of the loan, in the event of death, terminal illness or total permanent disability, whichever earlier.

But, that doesn’t mean this is your only option.

If you think you can get a better deal than the HPS, you are more than welcome to apply for a HPS exemption.

This brings us to the next point.

What is Mortgage Insurance (Private Insurer)?

Alternatively, you can consider getting your MRTA from private insurers.

You will find that private mortgage insurance can be cheaper than the HPS.

This is especially the case if you are buying an HDB flat together with your family member or partner as you will be issued two HPS policies instead of a joint one.

Also, both of you will have to pay your premiums separately.

In comparison, you can opt for joint policies if you choose private mortgage insurance which will usually be cheaper than two HPS policies.

You can use this HPS calculator from CPF to estimate the HPS premium amount to compare it with your mortgage insurance quote.

Not to mention that private mortgage insurance can cover both HDB flats and private property as well.

Here are the pros and cons of private mortgage insurance.

Pros:

- Greater scope: covers HDB flats and private property

- Transferrable: can be transferred to a new property if you decide to sell your home

- More affordable: typically cheaper than term insurance and HPS in some cases

- Add-on riders: flexibility to add coverage for critical illnesses, premium waivers, retrenchment coverage and more

- Flexible: can choose policy tenure.

Cons:

- Decreasing term assurance: sum assured is reduced each year in proportion to the loan amount and loan tenure of the assured while the premiums also tend to remain the same

- Limits on the sum assured: can only cover up to the total mortgage loan amount

- Cash only: you cannot use your CPF OA to pay for the premiums.

Which Is The Best Mortgage Insurance Plan To Get?

But ultimately, it boils down to your personal needs when it comes down to deciding which mortgage insurance plan to get.

Before diving straight into choosing one that suits you, here’s a reminder of the various definitions:

- Single Premiums are premiums that allow you to pay for your insurance in one lump sum

- Regular Premiums: Monthly premiums are the most common way to pay for insurance. In terms of frequency, there are several options for paying for your insurance; the most typical are annual or monthly premium payments.

Here are some mortgage insurance policies available in Singapore for you:

| Insurance | Maximum Sum Assured | Loan Tenure | Premium Term | Interest Rate |

| DBS eDecreasingTerm Mortgage Insurance (Single or Joint Life) | $500,000 | 5 – 35 years | Policy term less 2 years | 3% |

| Etiqa ePROTECT Mortgage Insurance (Single Life) | Amount of Housing Loan | 6 – 40 years | 90% of policy term | 1 – 4% |

| AIA Mortgage Reducing Term Assurance (Single or Joint Life) | Amount of Housing Loan | 10 years | 75% of policy term | 1 – 7% |

| AXA Decreasing Term Assurance Mortgage Insurance (Single or Joint Life) | $5,000,000 | 10 – 30 years | Single Premium: Full policy term

Regular Premium: 3 years |

1 – 15% |

| Great Eastern MortgageCare Mortgage (Single or Joint Life) | Amount of Housing Loan | 10 years | 80% of policy term | 5% |

| Manulife ManuProtect Decreasing (II) Mortgage Insurance (Single or Joint Life) | Amount of Housing Loan | 25 years | Full policy term | 1 – 5% |

| NTUC Income Mortgage Term Insurance (Single or Joint Life) | Amount of Housing Loan | 5 – 35 years | 2 years less than policy term | 1 – 7% |

| Prudential PRUMortgage Mortgage Insurance (Single or Joint Life) | Amount of Housing Loan | 10 – 35 years | 3 years less than policy term | 1 – 7% |

| Tokio Marine TM Mortgage Protection Insurance (Single or Joint Life) | Amount of Housing Loan | 10 – 30 years | 3 years less than policy term | 0 – 9.75% |

If you have questions about which Mortgage Insurance Plan to get after reading our real user reviews, why not ask our community of experts and experienced members at Seedly!

What is Term Life Insurance?

If you want more flexibility, you can opt for term life insurance to provide coverage for your home loans.

Term life insurance are insurance policies that offer protection for a fixed period of time. These policies typically pay out in the unfortunate event of death, terminal illness or total and permanent disability.

Here are some of the features of this type of insurance policy:

- Purpose: For Protection Safeguard

- Coverage: Cases of Death, Terminal Illness and total/permanent disability

- Period of Coverage: Variable or up to a certain age

- Guaranteed Death Benefit: Yes, Sum Assured

- Guaranteed Cash Value @ End: NIL

- Premiums: Regular Term

- Surrender Penalties: NIL

Unlike mortgage insurance, the coverage and premiums remain consistent throughout the policy term.

Here are some of the pros and cons of these policies:

Pros:

- Consistent: coverage and premiums remain the same during the policy period.

- Longer tenure: can cover you beyond the age of 65.

- Flexible benefits: benefits are paid out to the appointed beneficiary who can use the money in any way they wish.

- Tied to the individual: covers the person and not the property.

- Add-ons: flexibility to add additional coverage with a critical illnesses rider, premium waivers, retrenchment coverage and more.

Cons:

- Pricey: generally more expensive than the HPS and private mortgage insurance.

Which Is The Best Term Life Insurance Plan To Get?

To help you with your search, you can go on to Seedly to compare term life insurance plans and read our real user reviews.

Besides paying off their major debt, such as a mortgage. However, they should consider how much more would be needed to help a spouse or partner pay bills, support children, pay for college tuition or cover any other long-term needs, he says.

| Insurance | Maximum Sum Assured | Premium Term | Coverage |

| AIA DIRECT – AIA Term Cover Life Insurance | $400,000 | Renewable Term: 5 years

Fixed Term: 20 years or up to 65 years old |

Death, Terminal Illness and Total Permanent Disability |

| AIA Secure Flexi Term Life Insurance | $1,000,000 | Renewable Term: 5,10, 20 or 30 years

Fixed Term: up to 65, 75 or 100 years old |

Death, Terminal Illness and Terminal Cancer |

| AVIVA DIRECT Term Life Insurance | |||

| AXA DIRECT – Term Lite Life Insurance | $400,000 | Renewable Term: 5 years

Fixed Term: 20 years or up to 65 years old |

Death and Terminal Illness |

| AXA Term Protector Life Insurance | $2,000,000 | Renewable Term: 5,10, 20, 25 or 30 years

Fixed Term: 15 years or 99 years old |

Death, Terminal Illness and Total Permanent Disability |

| DBS TermProtect Life Insurance | $500,000 | Up to 40 years | Death, Terminal Illness and Total Permanent Disability |

| FWD Term Life Plus Insurance | $1,500,000 | Renewable Term: 5 years

Fixed Term: 5 years or up to 70 years old |

Death and Terminal Illness |

| Great Eastern DIRECT – Great Term Life Insurance | $400,000 | 20 years or up to 80 years old | Death, Terminal Illness and Total Permanent Disability |

| Great Eastern GoGreat Term Life Insurance | Plan 1: $100,000

Plan 2: $300,000 Plan 3: $500,000 |

Up to 65 years old | Death, Terminal Illness and Total Permanent Disability |

| Manulife DIRECT – ManuAssure Term Life Insurance | $400,000 | Renewable Term: 5 years

Fixed Term: 20 years or up to 65 years old |

Death, Terminal Illness and Total Permanent Disability |

| NTUC Income DIRECT Term Life Insurance | $400,000 | Renewable Term: 5 years

Fixed Term: 20 years or up to 64 years old |

Death, Terminal Illness and Total Permanent Disability |

| Prudential DIRECT – PRUProtect Term 5 Life Insurance | $400,000 | 5 years or up to 80 years old | Death, Terminal Illness and Total Permanent Disability |

| Singlife DIRECT – Singlife Term Life | $400,000 | Renewable Term: 5 years

Fixed Term: 20 years or up to 65 years old |

Death, Terminal Illness and Total Permanent Disability |

| Tiq DIRECT – Etiqa term Life Insurance | $400,000 | Renewable Term: 5 years

Fixed Term: 20 years or up to 70 years old |

Death |

| Tiq ePROTECT Term Life Insurance | $2,000,000 | Renewable Term: 5 yearsFixed Term: 20 years or up to 65 years old | Death |

| Tokio Marine DIRECT – TM Basic Term Life Insurance | $400,000 | Renewable Term: 5 yearsFixed Term: 20 years or up to 65 years old | Death, Terminal Illness and Total Permanent Disability |

| Tokio Marine TM Term Assure (II) Life Insurance | $2,000,000 | Renewable Term: 5, 10 yearsFixed Term: 11 years or up to 85 years old | Death, Terminal Illness and Total Permanent Disability |

Also, if you have any questions why not ask our community of experts and experienced members at Seedly!

Related Articles:

- Best Home Insurance (2022): Lessons Learnt When My Wife Tried to Set Me On Fire

- Insurance Policies You Need in Singapore For Each Age Group

- Insurance: How To Review & Why You Should

- Best Insurance Savings Plans in Singapore (2022): Dash PET vs Singlife Account vs Dash EasyEarn vs GIGANTIQ

- Best Insurance Options for Those With Pre-existing Conditions

Advertisement