With traditional bank savings accounts offering a paltry base interest of 0.05% p.a. and having multiple hoops to attain higher interest,

You might be looking for somewhere else to park your emergency fund or save up for a short-term financial goal.

Enter cash management accounts that offer stable, low-risk returns with high liquidity.

BUT, just like regular investments, these financial products are not capital-guaranteed by the Singapore Deposit Insurance Corporation (SDIC), and there is still a risk of losing your money.

Intrigued?

Here are some of the best cash management accounts for you to consider!

Disclaimer: We are not sponsored by any of these companies to write this article, even if we have promo codes included. Check out our Seedly Code of Ethics for more information. Information is accurate as of Jul 2026 . The information provided by Seedly serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any investment product. We are only covering SGD cash management accounts.

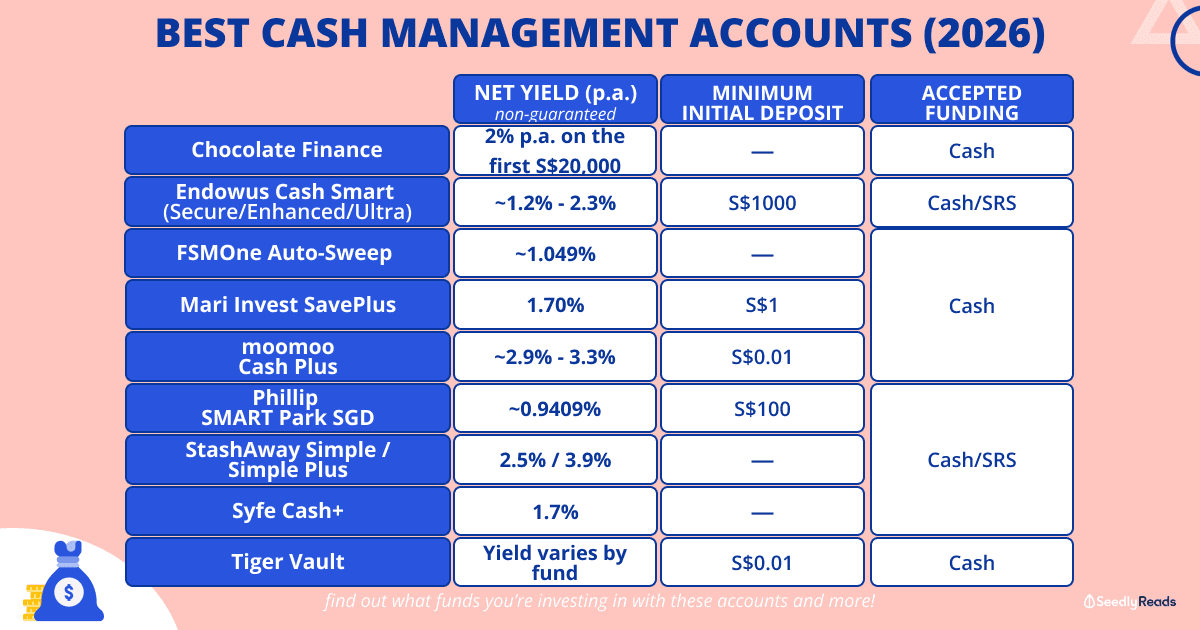

TL;DR: Best Cash Management Accounts in Singapore

| Account | Net Yield p.a. (Non-Guaranteed) | Minimum Initial Deposit | Funding Sources |

|---|---|---|---|

| Chocolate Finance | 2% p.a. on the first S$20,000; 1.8% p.a. on the next S$80,000; up to 1.8% thereafter | No deposit requirements | Cash |

| Endowus Cash Smart Secure | Approximately 1.2% to 1.3% p.a. net yield | S$1,000 | Cash | SRS |

| Endowus Cash Smart Enhanced | Approximately 1.9% p.a. net yield | ||

| Endowus Cash Smart Ultra | Approximately 2.3% p.a. net yield | ||

| FSMOne Auto-Sweep | Approximately 1.049% p.a. net yield | S$0 for auto-sweep; S$100 for manual deposits | Cash |

| Mari Invest SavePlus | 1.70% annualised over the past year; 2.80% annualised since launch, as at 31 May 2026 | S$1 | Cash |

| moomoo Cash Plus (SGD) | Approximately 2.9% to 3.3% p.a., depending on the selected | S$0.01 | Cash |

| Phillip Smart Park (SGD) | Approximately 0.9409% p.a. based on the seven-day rolling average | S$100 | Cash | SRS |

| StashAway Simple | Approximately 2.5% p.a. projected return | No deposit requirements | Cash | SRS |

| StashAway Simple Plus | Approximately 3.9% p.a. yield to maturity | ||

| Syfe Cash Flexi+ (SGD) | Approximately 1.7% p.a. projected net return | No deposit requirements | Cash | SRS |

| Tiger Brokers Tiger Vault (SGD) | Yield varies by fund | From S$0.01 for selected funds | Cash |

All rates and returns are subject to change. Moreover, projected returns, historical performance, annualised yields and yield-to-maturity figures are not directly comparable.

In general:

- For a straightforward account with tiered returns and a current SingSaver reward, consider Chocolate Finance.

- For several risk levels within one platform, consider Endowus Cash Smart.

- For a low minimum starting amount, consider Mari Invest SavePlus, moomoo Cash Plus or Tiger Vault.

- For flexible next-day withdrawals, consider Syfe Cash+ Flexi.

- For SRS funds, consider Endowus Cash Smart, Phillip SMART Park, StashAway Simple, StashAway Simple Plus or Syfe Cash+ Flexi SRS.

- Meanwhile, if you already use a brokerage, its built-in cash-management facility may be more convenient than opening another account.

We will be comparing these cash management services based on the following criteria:

- Interest rate (or yields)

- Minimum Initial Deposit

- Fees

- Liquidity

- Underlying Funds

- Risk (% drawdowns where available).

Click to Teleport:

- What’s the difference between a cash management account and savings account?

- How safe are cash management accounts: What are the underlying funds?

- Chocolate Finance

- Endowus Cash Smart Secure

- Endowus Cash Smart Enhanced

- Endowus Cash Smart Ultra

- FSMOne Auto-Sweep

- Mari Invest

- moomoo Cash Plus (SGD)

- Phillip Smart Park (SGD)

- StashAway Simple

- StashAway Simple Plus

- Syfe Cash+

- Tiger Vault (SGD)

What Is the Difference Between a Cash Management Account and a Savings Account?

A savings account is a bank-deposit product. In contrast, a cash management account is usually an investment solution offered by a digital wealth platform, fund distributor or brokerage.

Your bank pays interest on your savings balance. Meanwhile, a cash management platform generally invests your money in one or more underlying funds.

As a result, cash management returns can change according to money-market rates, bond yields and fund performance.

Additionally, bank deposits with participating institutions may receive Deposit Insurance Scheme protection within the applicable limits. Cash management investments, however, are generally not covered.

Therefore, you should not assume that a cash management account is as safe as a bank deposit simply because its value appears stable.

Cash management accounts may be useful for:

- Money set aside for a short-term goal

- Part of an emergency fund that you do not need immediately

- Cash waiting to be invested

- SRS money awaiting deployment

- Spare brokerage cash

However, you should still keep enough readily accessible money in a bank account for bills and genuine emergencies.

How Safe Are Cash Management Accounts: Underlying Funds Risk Profile Comparison

Is a cash management account safe?

Generally, these products are considered relatively low risk. Nevertheless, “low risk” does not mean “no risk”.

The level of risk mainly depends on what the account invests in.

Cash Fund (Safest)

Cash funds are the safest asset class among these three funds in the fund space. The fund generally invests in a diversified portfolio of safe institutional bank fixed deposits and treasury bills for this asset class and has the lowest downside risk compared to the other two funds.

For example, the Fullerton SGD Cash Fund is a cash fund that invests in safe income instruments like Singapore Dollar (SGD) Deposits with Singapore-registered banks and Singapore Government Treasury Bills.

These deposits have varying terms of maturity, not more than 366 working days.

Fun fact: the Fullerton Cash Fund had never seen a day of negative returns since inception.

Money Market Fund (Less Safe): Singapore Money Market Fund and More

Money-market funds invest in short-term deposits and high-quality money-market instruments. Additionally, some may hold short-term government or corporate debt.

These funds usually aim to preserve liquidity and produce returns aligned with prevailing short-term interest rates.

Nevertheless, money-market-fund yields can fall when central-bank rates decline. This has become particularly relevant in 2026, as yields have generally moved lower following interest-rate cuts.

Short-Term Bond Fund (Least Safe)

Short-duration bond funds generally take more interest-rate and credit risk than pure cash or money-market funds.

Consequently, they may offer higher potential yields. However, their unit prices can fall when market interest rates rise or credit spreads widen.

For this reason, products such as Endowus Cash Smart Ultra and StashAway Simple Plus may be less suitable for money you need within the next few months.

Chocolate Finance

Chocolate Finance is a cash-management platform operated by Chocfin Pte Ltd, which is licensed and regulated by the Monetary Authority of Singapore for fund-management activities.

Chocolate Finance SGD Returns

Chocolate Finance currently advertises:

- 2% p.a. on the first S$20,000

- 1.8% p.a. on the next S$80,000

- Up to 1.8% p.a. on balances above S$100,000

The stated returns are supported under the Chocolate Top-Up Programme during the applicable qualifying period.

However, the programme does not make your investment capital-guaranteed. Instead, Chocolate Finance may top up the returns delivered by the underlying portfolio according to its prevailing programme terms.

Minimum Initial Deposit

Chocolate Finance does not state a standard minimum deposit.

Therefore, it may be accessible to someone who wants to begin with a smaller amount.

Fees

Chocolate Finance states that it does not charge users a standard management fee.

Instead, the platform earns when the underlying portfolio performs above the returns delivered to users under the Chocolate Top-Up Programme.

Underlying Funds

Chocolate Finance invests through a managed portfolio of fixed-income and short-duration investment strategies.

However, its portfolio composition may change as the platform manages interest-rate, duration and credit risks. Therefore, check the latest allocation in the Chocolate Finance app before depositing.

Liquidity

There is no formal lock-in period, and users can submit withdrawals through the app.

However, withdrawal speed and instant-withdrawal limits may be affected by transaction limits, operational conditions or the amount being withdrawn.

Risk

Chocolate Finance is not a bank account. Therefore, the balance is not covered by the Deposit Insurance Scheme.

Although client assets are held separately from the company’s operating assets, the underlying investments can still rise or fall in value.

SingSaver Chocolate Finance Promotion

New customers who apply through SingSaver can receive:

- Up to S$120 cash via PayNow, or

- Up to S$130 in Grab vouchers

To qualify, you must make a first deposit of at least S$1,000 and maintain the required amount for 60 days.

Terms and conditions apply.

Endowus Cash Smart

Endowus Cash Smart provides three portfolios with different risk-and-return profiles:

- Cash Smart Secure

- Cash Smart Enhanced

- Cash Smart Ultra

All three portfolios invest in combinations of cash, money-market and short-duration fixed-income funds.

Moreover, Endowus rebates trailer fees received from fund managers back to clients.

Endowus Cash Smart Secure

Cash Smart Secure is the lowest-risk option in the range.

Endowus Cash Smart Secure Net Yield

The latest available figures place its net yield at approximately 1.2% to 1.3% p.a.

However, this is not a fixed rate. Instead, the yield changes with the underlying funds and prevailing money-market conditions.

Minimum Initial Deposit

The minimum initial investment is S$1,000.

Fees

Endowus charges an access fee of 0.15% p.a.

In addition, the underlying funds charge fund-level fees. Nevertheless, the net yield displayed by Endowus is generally shown after fund-level fees and trailer-fee rebates.

Underlying Funds

Cash Smart Secure holds a diversified portfolio of cash and money-market funds.

Because portfolio allocations can change, refer to the current Endowus portfolio page rather than relying on a fixed allocation table.

Liquidity

There is no formal lock-up.

However, withdrawals are not instant. Depending on fund settlement and bank processing, receiving your money may take several business days.

Risk

Secure is the lowest-risk Cash Smart portfolio. Nevertheless, it remains an investment product, so its value and yield are not guaranteed.

Endowus Cash Smart Enhanced

Cash Smart Enhanced takes somewhat more risk in exchange for a higher potential yield.

Endowus Cash Smart Enhanced Net Yield

The current displayed net yield is approximately 1.9% p.a.

However, this figure can change as market yields and portfolio holdings change.

Fees

The Endowus access fee is 0.15% p.a., while fund-level fees are deducted within the underlying funds.

Underlying Funds

Enhanced combines money-market funds with high-quality short-duration bond funds.

Therefore, it may experience more price movement than Cash Smart Secure.

Risk

Enhanced may be suitable for money that you can leave invested for longer.

However, you should be prepared for occasional negative daily or monthly returns, especially when bond yields rise sharply.

The minimum investment and general withdrawal process are similar to those for Cash Smart Secure.

Endowus Cash Smart Ultra

Cash Smart Ultra takes the most investment risk among the three Cash Smart portfolios.

Endowus Cash Smart Ultra Net Yield

The latest displayed net yield is approximately 2.3% p.a.

Although this is higher than the other two Cash Smart options, it is neither fixed nor guaranteed.

Fees

The Endowus access fee remains 0.15% p.a., excluding underlying fund-level costs.

Underlying Funds

Ultra invests mainly in high-quality short-duration bond and money-market funds.

Consequently, the portfolio can be more sensitive to changes in bond yields and credit conditions.

Risk

Cash Smart Ultra can experience larger short-term fluctuations than Secure or Enhanced.

Therefore, it may not be the best place to keep money required for an expense in the next few months.

FSMOne Auto-Sweep Account

![]()

The FSMOne Auto-Sweep Account is designed for existing FSMOne brokerage customers.

Once you opt in, eligible idle money in your brokerage cash account can be swept automatically into an underlying cash-management portfolio.

Additionally, the balance can be used to fund eligible investments on FSMOne. Therefore, the product may be convenient if you regularly buy funds, shares or other investments through the platform.

FSMOne Auto-Sweep Net Yield

FSMOne Auto-Sweep currently provides a net yield of approximately 1.049% p.a.

However, the yield is variable and may change according to the performance of the underlying funds and prevailing market rates.

Minimum Initial Deposit

There is no minimum deposit for eligible funds moved through the automatic sweep function.

However, a minimum of S$100 applies when you make a manual investment.

Fees

FSMOne charges a fee of 0.05% per quarter, equivalent to approximately 0.20% p.a.

The reported net yield should therefore be reviewed together with the product’s expenses and underlying fund performance.

Liquidity

The product is designed to provide liquidity for investments made through FSMOne.

However, bank withdrawals and fund settlement may require additional processing time.

Underlying Funds

The portfolio invests primarily in cash and money-market funds.

Nevertheless, its allocation and individual fund holdings may change. Therefore, check the latest factsheet or FSMOne platform information before investing.

Risk

FSMOne Auto-Sweep is an investment product rather than a deposit account.

As a result, returns are not guaranteed, and the balance is generally not covered by deposit insurance.

Mari Invest SavePlus

Mari Invest SavePlus gives MariBank users access to the Lion-MariBank SavePlus Fund.

It is a money-market-oriented investment product rather than a MariBank savings deposit.

Mari Invest SavePlus Returns

As at 31 May 2026, MariBank reported:

- 1.70% annualised return over the past year

- 2.80% annualised return since the fund’s launch

These figures show historical performance. Therefore, they should not be interpreted as the return you will receive over the next year.

Minimum Initial Deposit

You can start from S$1.

Consequently, SavePlus is one of the most accessible products in this comparison.

Fees

MariBank does not charge a separate transaction or platform fee for SavePlus.

However, the underlying Lion-MariBank SavePlus Fund charges an annual management or fund fee of approximately 0.25% p.a.

This fee is reflected in the fund’s net asset value and published returns.

Liquidity

You can make an instant withdrawal of up to S$10,000 per day directly into your MariSavings Account.

However, larger withdrawals or transactions submitted under certain circumstances may take longer to process.

Underlying Fund

SavePlus invests through the Lion-MariBank SavePlus Fund, which is managed by Lion Global Investors.

Risk

SavePlus is not a MariBank deposit.

Therefore, it is not covered by deposit insurance, and returns can be negative on individual days.

moomoo Cash Plus

We have another animal-themed financial institution in the shape of moomoo Singapore’s Cash Plus cash management account.

![]()

To access this account, you must sign up for a moomoo Singapore brokerage account and opt-in for moomoo Cash Plus.

moomoo Cash Plus Yield

Core Singapore-dollar money-market funds available through moomoo Cash Plus currently provide base annualised yields of approximately 2.9% to 3.3% p.a.

However, the exact return depends on the specific fund selected and changes with market conditions.

Additionally, moomoo may advertise higher promotional rates, such as 6.8% p.a., to eligible new users. These rates usually include temporary yield boosters and only apply to a limited balance or promotional period.

Therefore, compare the underlying fund’s standard yield separately from any welcome campaign.

Minimum Initial Deposit

Certain Cash Plus funds can be accessed from approximately S$0.01, although the minimum may vary by fund.

Fees

Subscription, redemption and platform fees may be waived for selected Cash Plus funds.

Nevertheless, each underlying fund has its own expense ratio, which is reflected in its net asset value and published returns.

Liquidity

Cash Plus redemptions are generally processed within T+0 to T+1 into the moomoo brokerage account, depending on the fund.

After that, transferring money from the brokerage account to your bank may take additional time.

Risk

The level of risk depends on the chosen fund.

Although money-market funds are generally low risk, returns are not guaranteed and losses remain possible.

Phillip SMART Park

Phillip SMART Park allows POEMS customers to place idle brokerage cash into the Phillip Money Market Fund.

Phillip SMART Park SGD Return

Phillip SMART Park currently provides a return of approximately 0.9409% p.a., based on its seven-day rolling average.

However, the return is variable and may change as the underlying money-market fund’s yield changes.

Fees

The Phillip Money Market Fund has an internal expense ratio of approximately 0.45% p.a.

This expense is deducted within the fund and is reflected in its net asset value and reported performance.

Minimum Initial Deposit

The minimum initial investment is approximately S$100.

Liquidity

SMART Park has no formal long-term lock-in.

Eligible withdrawal instructions submitted before the provider’s cut-off may generally be processed by the next business day.

Underlying Fund

SGD balances are invested in the Phillip Money Market Fund.

The fund primarily invests in short-term money-market instruments and debt securities.

Cash and SRS

Phillip SMART Park supports both cash and SRS funds.

Therefore, it may be useful for POEMS customers who want to earn a potential return on idle SRS money before deploying it into longer-term investments.

Risk

Although the Phillip Money Market Fund is considered relatively low risk, it remains an investment product.

Consequently, returns and capital are not guaranteed.

StashAway Simple

StashAway Simple is an ultra-low-risk cash-management portfolio.

StashAway Simple Projected Return

StashAway currently advertises a projected return of approximately 2.5% p.a.

However, the return is not guaranteed and may change as short-term market rates move.

Minimum Deposit

No standard minimum deposit is prominently stated.

Therefore, the account may be suitable for readers who want to start with a smaller amount.

Fees

StashAway does not charge a separate management fee for Simple.

Nevertheless, the underlying funds charge expense ratios, which are reflected in the projected net return.

Liquidity

There is no lock-in period or withdrawal penalty.

However, withdrawing cash to your bank account generally takes several business days.

Underlying Funds

Simple invests in:

- LionGlobal SGD Money Market Fund

- LionGlobal SGD Enhanced Liquidity Fund

The portfolio has historically used an allocation of approximately 30% and 70% respectively.

However, always confirm the current allocation on StashAway’s product page.

Cash and SRS

StashAway Simple is available for cash and SRS funds.

SingSaver StashAway Promotion

New StashAway customers who apply through SingSaver can receive 1,900 Max Miles by HeyMax, worth S$34.20.

To qualify, fund either:

- At least S$500 into an eligible investment portfolio, or

- At least S$2,000 into a cash-management portfolio

Terms and conditions apply.

StashAway Simple Plus

Simple Plus aims to deliver a higher potential return than Simple.

However, it invests in instruments with greater duration and price risk. Therefore, its value may fluctuate more in the short term.

StashAway Simple Plus Yield to Maturity

StashAway currently advertises approximately 3.9% p.a. yield to maturity.

Yield to maturity is not the same as a guaranteed annual return. Instead, it estimates the return of the underlying bonds if they are held until maturity and assumptions such as reinvestment and no default hold.

Recommended Holding Period

StashAway recommends holding Simple Plus for at least 12 months.

Consequently, it may not be suitable for an emergency fund that you could need next week.

Minimum Deposit

No standard minimum deposit or earnings cap is prominently stated.

Fees

There is no separate StashAway management fee for Simple Plus.

However, underlying fund-level expenses apply and are reflected in its return calculations.

Liquidity

There is no formal lock-in.

Nevertheless, selling during an unfavourable market period may result in a lower return or capital loss.

Risk

Simple Plus carries more interest-rate and credit risk than StashAway Simple.

Therefore, compare the higher potential yield against the possibility of short-term volatility.

Syfe Cash Flexi+ (SGD)

Also, we have the Syfe Cash Flexi+ account by Syfe.

![]()

To access this, you must sign up for an account with Syfe.

Syfe Cash+ Flexi is a low-risk cash-management portfolio offered in SGD and USD.

This comparison focuses on its SGD option.

Syfe Cash+ Flexi SGD Projected Net Return

Syfe Cash+ Flexi SGD currently provides a projected net return of approximately 1.7% p.a.

The portfolio combines the LionGlobal SGD Money Market Fund and LionGlobal SGD Enhanced Liquidity Fund.

As a result, its projected return can be higher than a pure money-market strategy while remaining relatively liquid.

However, the projected net return is not guaranteed and may change with Singapore money-market and short-duration bond yields.

Minimum Initial Deposit

There is no minimum portfolio funding requirement for Cash+ Flexi SGD.

Fees

Syfe charges a management fee of approximately 0.05% to 0.15% p.a., depending on the client’s pricing tier.

Additionally, the underlying funds charge fund-level expenses. These costs and any applicable trailer-fee rebates are reflected in the projected net return.

Liquidity

There is no lock-in period.

Syfe currently advertises unlimited next-day withdrawals. Nevertheless, actual bank-crediting times may depend on when you submit the request and whether it falls on a business day.

Underlying Funds

The portfolio uses an allocation of approximately:

- 30% LionGlobal SGD Money Market Fund

- 70% LionGlobal SGD Enhanced Liquidity Fund

However, Syfe may adjust the portfolio allocation when market conditions or investment assumptions change.

Cash and SRS

Cash+ Flexi is available for cash.

Additionally, Syfe offers an SRS-eligible Cash+ Flexi portfolio.

SingSaver Syfe Promotion

SingSaver may offer rewards for eligible new or previously unfunded Syfe customers who deposit at least S$2,000 into selected Syfe products.

However, eligibility may differ between brokerage, managed-investment and cash-management products. Therefore, check the current campaign terms before applying.

Tiger Brokers Tiger Vault

Last but not least, we have the Tiger Brokers cash management account.

To access the Tiger Vault, you must sign up for a brokerage account with Tiger Brokers.

Tiger Vault allows you to pick between the SGD or USD MMFs.

Tiger Vault SGD Yield

Tiger Vault’s return depends on the fund selected.

Although its product page may advertise higher “up to” rates, these headline figures can include temporary yield boosters.

Therefore, compare the underlying fund’s prevailing seven-day annualised yield instead of relying only on the promotional headline.

Minimum Initial Deposit

Selected Tiger Vault funds allow you to start from as little as S$0.01.

However, the minimum investment may differ according to the specific money-market fund selected.

Underlying Funds

Available SGD options may include funds managed by providers such as:

- Fullerton Fund Management

- Lion Global Investors

- UOB Asset Management

However, the live fund list may change.

Fees

Tiger Vault may waive platform, subscription or redemption charges for selected funds.

Nevertheless, the underlying funds charge expense ratios, which reduce the returns earned.

Liquidity

There is no fixed long-term lock-in for standard money-market funds.

However, fund redemption and the subsequent bank withdrawal can take several business days.

Risk

The level of risk depends on the underlying fund.

Therefore, review its portfolio, duration, credit quality, expense ratio and historical volatility before subscribing.

Closing Thoughts

So, which is the best cash management account in Singapore?

There is no single account that is best for everyone.

Instead, the right option depends on how soon you need the money, which platform you already use and how much fluctuation you are prepared to accept.

For example, Chocolate Finance may appeal to someone who wants a simple tiered return and a current SingSaver reward. Meanwhile, StashAway Simple may suit someone who prefers an ultra-low-risk portfolio with no formal lock-in.

On the other hand, Endowus Cash Smart Enhanced, Endowus Cash Smart Ultra and StashAway Simple Plus may offer higher potential yields. However, they can experience more short-term volatility.

Additionally, brokerage-based products such as moomoo Cash Plus, FSMOne Auto-Sweep, Phillip SMART Park and Tiger Vault may be convenient if you already invest through those platforms.

Before choosing, ask yourself:

- When will I need this money?

- Can I wait several business days for a withdrawal?

- Is the displayed figure projected, historical, promotional or guaranteed?

- Could I tolerate a temporary loss?

- Am I paying platform or underlying fund fees?

- Is the product covered by deposit insurance?

Most importantly, do not chase the highest displayed rate without understanding how it is calculated.

A promotional 6.8% p.a. campaign, for instance, is not directly comparable with a standard money-market-fund yield. Similarly, a yield-to-maturity figure is not the same as a guaranteed return.

Therefore, always compare the standard rate, qualifying balance, promotional period, investment risk and withdrawal terms before deciding where to place your cash.

Read More

Advertisement